Beyond the Model: The $400 Billion AI Gamble is Now About Architecture, Not IQ

Part II - The End of the Giant Brain: How the AI Infrastructure Wars Are Redefining Intelligence

This article is Part II, to “The Death of the Giant Brain”, which you can read here. It will be a short follow-on piece, simply to say - you can follow the breadcrumbs, to figure out the strategy:

The Death of the Giant Brain

Not too long ago, the consensus was clear: the future belonged to whoever built the biggest, longest-context, smartest single model. A 1M-token context window was the gold standard. The dream was any model so vast it could hold your entire codebase, your entire document corpus, your entire

It takes into consideration prior articles and several recent presentations by Benedict Evans, “AI Eats The World” and his prior presentation in Singapore.

Note: All images courtesy of Nano Banana Pro

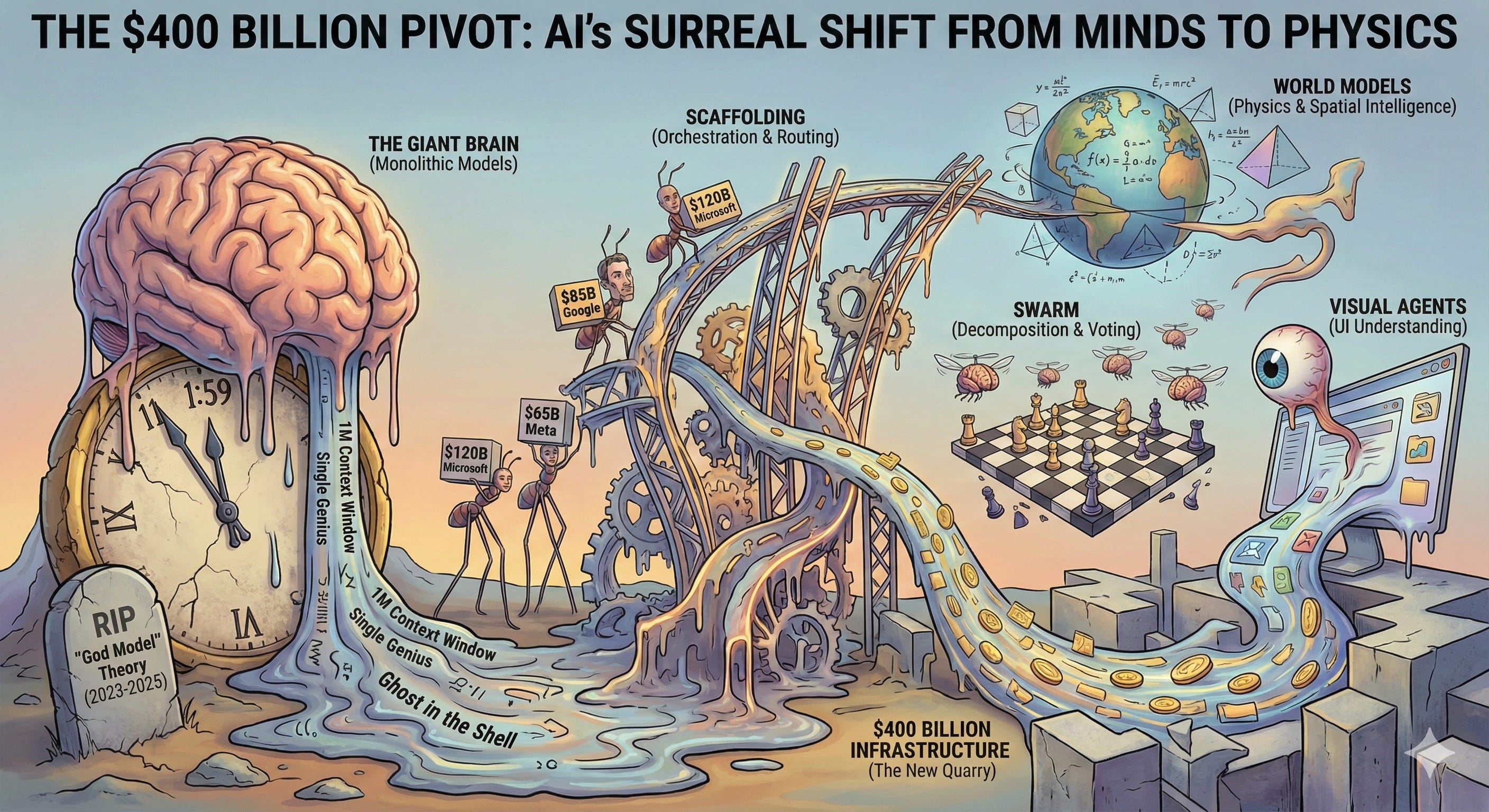

The $400 Billion Pivot: Why the AI Wars Just Shifted from Minds to Physics

If you blinked between November 12th and November 18th, you missed a revolution. I am guessing, in one form or another, we felt it’s effects. In a span of 144 hours, OpenAI launched GPT-5.1, Google countered with Gemini 3, and the industry effectively reset the board.

In Part I: The Death of the Giant Brain, I documented how the industry quietly admitted that a single, monolithic model cannot “think” its way through complex problems without help. The solution was decomposition—breaking big problems into small pieces for agentic swarms.

But if Part I was about the software of intelligence, Part II is about the physics of the industry.

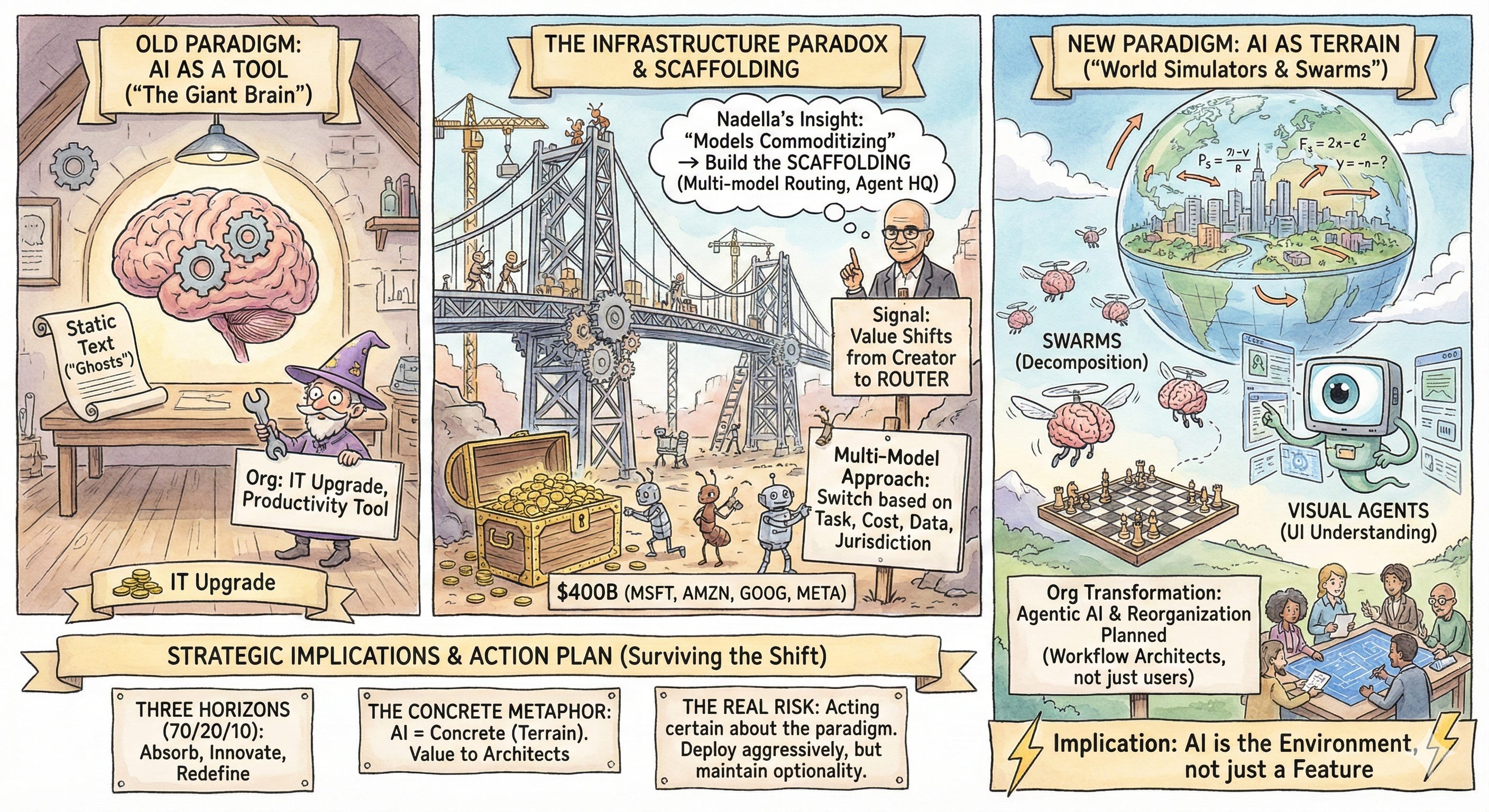

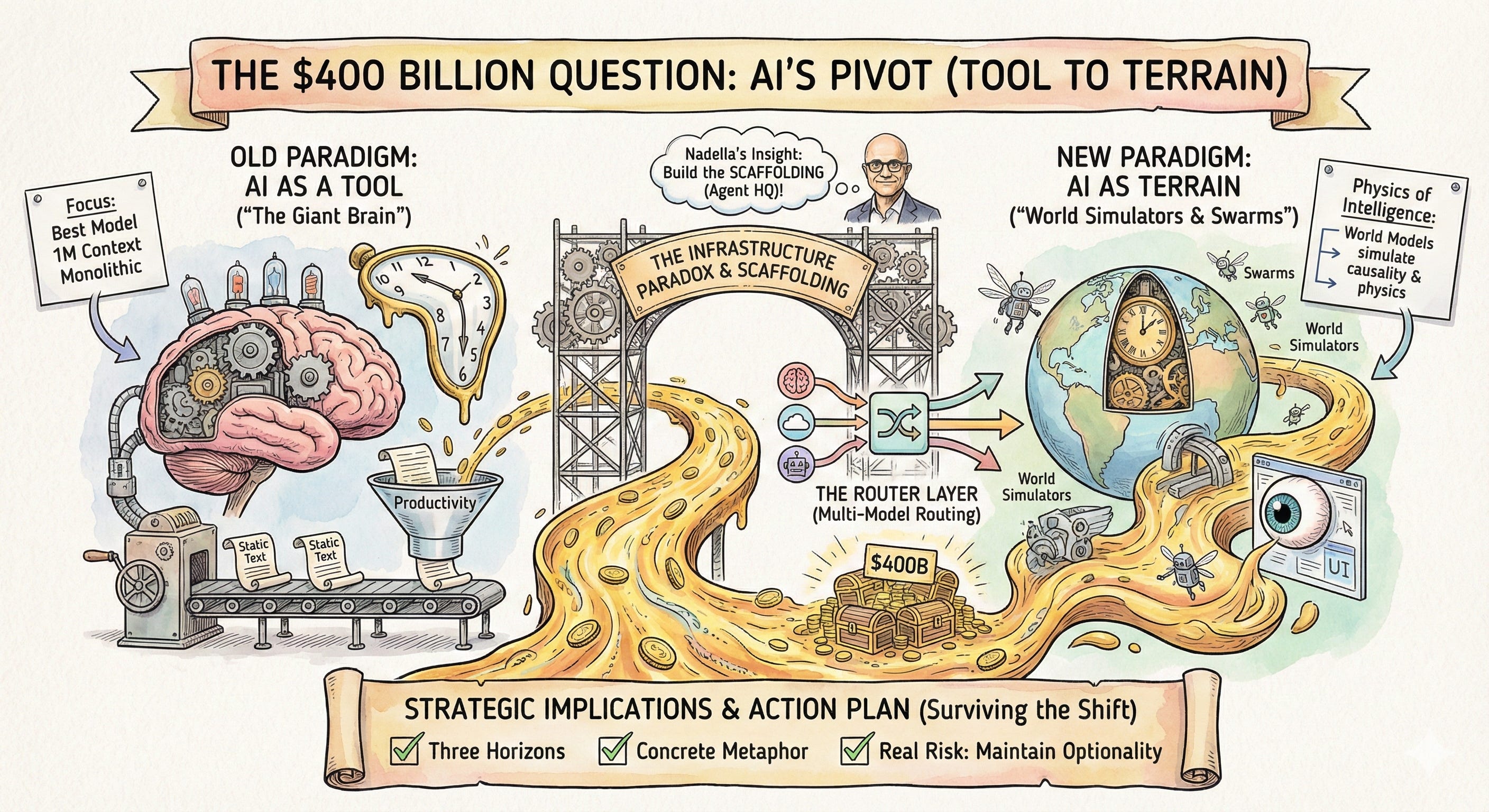

We are currently witnessing the most expensive infrastructure buildout since the telecommunications boom—approaching $400 billion in 2025 alone. But here is the twist that most observers, I believe, are possibly missing: The money isn’t being spent to build a better chatbot. It is being spent to turn AI from a tool into the terrain itself.

I. The Infrastructure Paradox

The numbers, as we know the, are staggering. Microsoft is spending $120 billion this year. Amazon is matching them. Combined with Google and Meta, Big Tech is deploying capital equivalent to 2% of the U.S. GDP.

To the casual observer, this looks like an arms race for the “smartest” model. But listen closer to the generals.

In an interview well worth watching (or re-watching) with Dwarkesh Patel earlier this year, Microsoft CEO Satya Nadella said the quiet part out loud: “I do believe the models are becoming commoditized”.

This creates a massive paradox: Why spend $120 billion on infrastructure if the core product—intelligence—is racing toward zero marginal cost?

The answer lies in what Nadella calls the “Scaffolding.” The bet isn’t on owning the electricity (the model); it’s on owning the grid (the orchestration). The comparison to electricity has been made umteenth times. We know Nadella is aggressively pursuing a multi-model strategy—integrating Anthropic’s Claude, OpenAI’s GPT, and Meta’s Llama into a single “Agent HQ”.

The Signal: The value capture is shifting from the creator of the intelligence to the router of the intelligence. In 2026, the most powerful company won’t be the one with the highest IQ model; it will be the one that decides which model gets the job.

II. The Physics of Intelligence: From “Ghosts” to World Models

For five years, skeptics have rightly called LLMs “ghosts”—statistical mirrors of human text that understand language but not the physical world. They could write a poem about an apple, but they couldn’t understand why it falls.

On September 30, 2025, that distinction blurred. But the shift goes far beyond OpenAI. We are seeing the rise of “World Models”—systems that don’t just predict the next token, but simulate the next second of reality.

The Rise of Spatial Intelligence

The most critical development of Q4 wasn’t a chatbot; In my mind, it was the launch of Marble by World Labs, the spatial intelligence startup founded by “Godmother of AI” Fei-Fei Li.

World Labs posits that true intelligence requires “Spatial Intelligence”—the ability to reason about 3D space, physics, and consequence. Unlike GPT-5.1, which lives in a text box, Marble is a Large World Model (LWM). It understands that a cup on a table has weight, friction, and fragility.

As Li explained at the launch, “We are moving from AI that can see and talk, to AI that can do”. The DeepMind team started earlier, as I describe below.

Google’s Simulation Bet

Google DeepMind is running the same play but at an industrial scale. Alongside Gemini 3, they released updates to Genie (Generative Interactive Environments) and SIMA 2.

Genie isn’t a video generator; it’s a physics engine learned entirely from video data. It allows Google to train agents in a “dream” version of the world before deploying them in the real one.

The Application: You don’t train a $100,000 robot in a real factory where it might break something. You train it in a Genie/SIMA 2 simulation where it can fail a million times in a virtual second.

Why this changes the roadmap: If we can simulate physics reliably, AI stops being a tool for writing and becomes a sandbox for doing. The $400 billion infrastructure isn’t just storing text; it is modeling reality to serve as a training ground for the physical economy.

III. The “Concrete” Moment

The best metaphor for this moment isn’t the discovery of electricity. It is the invention of concrete.

When concrete was popularized, it didn’t just make houses cheaper; it fundamentally changed what could be built. When reinforced with steel, it allowed for skyscrapers, dams, and highways to be built. Crucially, the competitive advantage didn’t go to the people who owned the cement mixers. It went to the architects who understood the new structural possibilities.

We are leaving the “Cement Mixer” phase (building models) and entering the “Architecture” phase (building organizations).

The Org Chart is the New Tech Stack

Most organizations are still treating AI as an IT upgrade—installing “Copilot” and hoping for productivity gains. This is a mistake.

As Nadella outlined at Microsoft Ignite, we are moving toward “Agentic AI”—systems that don’t just answer questions but execute workflows. This requires a fundamental reorganization of human talent:

Old Role: Junior Analyst (pulls data, writes report).

New Role: Workflow Architect (designs the agent swarm, verifies the output).

The “Deployment Gap” is real. While 95% of companies are stuck in “Horizon 1” (using AI for summaries and emails), the winners are moving to “Horizon 2”—deploying multi-agent systems that reshape entire departments.

IV. The Strategy: How to Survive the Shift

For the CIO or CFO reading this, the path forward requires abandoning the “One Model to Rule Them All” mentality.

1. Build the “Router” Layer Do not lock your organization into a single model provider. Build an orchestration layer that routes tasks based on complexity and cost. Use Gemini 3 Pro for deep reasoning, Claude Sonnet for nuance, and specialized World Models for physical simulation tasks.

2. Focus on “Visual Agents” Gemini 3’s 72.7% score on ScreenSpot-Pro (UI understanding) signals that AI can now “see” your legacy software. You no longer need an API for everything. Prepare for agents that can navigate your GUI like a human.

3. Don’t Buy the Cement, Build the Blueprint Stop waiting for the “perfect” model. The models are now commodities. The scarce resource is the organizational capacity to integrate them into agentic workflows.

The Verdict: The Giant Brain is dead (Part I). The Terrain has shifted (Part II). The future belongs to those who stop waiting for a smarter god and start building a better swarm.

Note: All Images, courtesy of Nano Banana Pro

References & Further Reading

Infrastructure & Economics

World Models & Spatial Intelligence

[4] Marble: A Multimodal World Model, World Labs (Nov 12, 2025). Link

[5] Fei-Fei Li’s World Labs Surpasses $1 Billion Valuation, Humans of Globe (Jul 2024). Link

[6] SIMA 2: An Agent that Plays, Reasons, and Learns With You in Virtual 3D Worlds, Google DeepMind Research (Nov 2025). Link

[7] Genie: Generative Interactive Environments, Google DeepMind (Feb 2024). Link

[8] Learning Interactive Real-World Simulator (UniSim), Google DeepMind (ICLR 2024). Link

Noted References:

Nadella on the “Commoditization” of Models:

Satya Nadella Debates the Future of Microsoft and AI, Dwarkesh Patel Podcast (Feb 2025). Link

The Infrastructure Numbers:

The “World Simulator” Shift:

The Model War (Gemini 3 vs GPT-5.1):

Microsoft’s Multi-Model Pivot:

Satya Nadella says “our multi-model approach goes beyond choice”, ITPro (Sep 2025). Link

Meta’s Infrastructure Play:

Meta Announces SAM 3, FB News (Nov 2025). Link