Infinite Demand vs. Capital Velocity

A Very Little Dive into the "Scaling Laws" of AI Economics

Ethan Choi’s 2026 analysis on “Who Wins The AI Race?” is essentially a “State of the Union” for the AI era. Well worth the read because the points are succinctly captured and threaded together, with all the relevant references. One could assume he moves past the AI hype to look at the cold, hard math of power, infrastructure, and revenue.

Unfortunately, that article doesn’t quite do so. Obviously, I have questions about a few critical points that, from any investor’s perspective, should be thoroughly considered.

In essence, here’s a breakdown of his most interesting points (to me at least), organized for strategic usefulness, from this source.

1. The “Gigawatt Standard”: AI’s New Currency

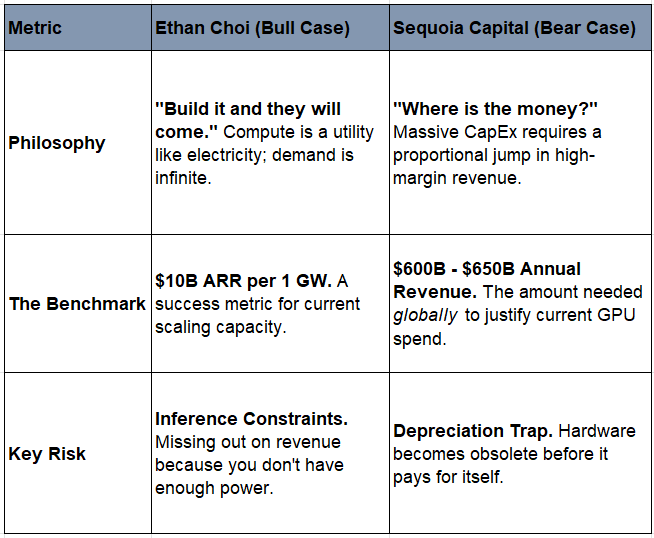

Choi argues that we should stop measuring AI companies by user count and start measuring them by Gigawatts (GW) of secured power. Power is the ultimate “bottleneck” to revenue.

The 1 GW Economic Unit:

Revenue: 1 GW of data center capacity generates roughly $10B in ARR.

Reach: It supports approximately 400M Weekly Active Users (WAU).

Training vs. Inference: Currently, much of the GW capacity is “locked” in training. The winner of the race is whoever transitions most of their GW to Inference (revenue-generating usage) first.

The Scorecard:

OpenAI: ~2.0 GW (~$20B ARR)

Anthropic: ~0.9 GW (~$9B ARR)

xAI (Grok): 1.0 GW (High capacity, but low ARR as it’s currently optimized for training).

2. The Adoption Gap: Why We Aren’t “Late”

Choi dismisses the idea that the AI bubble is bursting. He uses a “Innings” metaphor to show how early we actually are.

16% Penetration: While it feels like everyone uses ChatGPT, only 16% of the global population are GenAI users. To reach internet-level ubiquity (75%), we need a 5x growth in infrastructure.

The “Horizontal” Agent Era: We are currently in the “Departmental” phase (AI for just Support, or just Legal). The next phase is “Horizontal,” where agents like Glean or OpenAI’s Operator work across every department 24/7 without “cigarette breaks or PTO.”

Infinite Demand: Unlike social media (where there are only so many hours in a day), the demand for intelligence and automated labor is theoretically infinite.

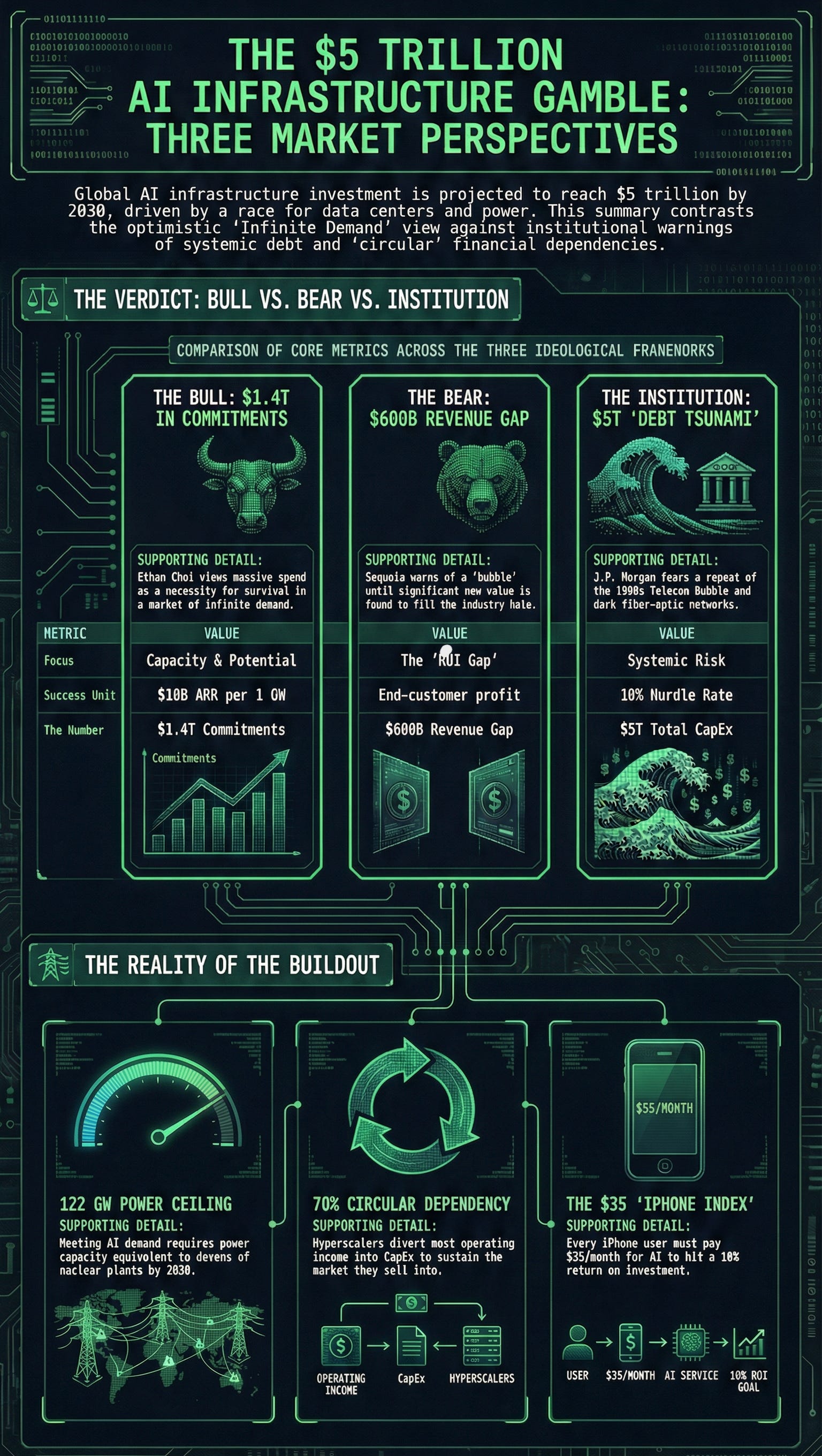

3. The $1.4 Trillion “Web of Deals”

The most misunderstood part of the 2026 landscape is OpenAI’s spending. Choi clarifies that OpenAI isn’t “burning” $1.4T; they are “orchestrating” a massive infrastructure web.

Capex vs. Opex:

$800B (Partners): Companies like Microsoft, Oracle, and MGX pay to build the physical data centers.

$600B (OpenAI): This is a long-term “Inference Commitment”—essentially a promise to pay rent over 10 years to use that power.

The Speed Gap: Hyperscalers (AWS/Google) took 15 years to build 10 GW. The AI labs are trying to build 30 GW in 5 years.

4. Model Wars: The “Vibe” Shift

Choi notes that “which model is best” is now a bad question. Performance fluctuates like a horse race.

The 2025/26 Flip: Google (Gemini 3) and Anthropic (Claude 4.5) currently hold the technical lead, causing a “Code Red” at OpenAI.

The “Basket of Partners”: Because model leads shift so fast, investors should look at the infrastructure layer (Nvidia, AMD, Broadcom) rather than betting on a single “winning” model.

Specialization: Founders are no longer using one model. They “mix and match”—using Claude for code, Gemini for long-context research, and GPT for general reasoning.

5. The “White-Collar” Protest Warning

A unique point Choi raises is the social impact of this specific scale of buildout.

Shift in Unrest: He predicts that 2026 will see the first major anti-AI protests from white-collar workers, not blue-collar. As “Horizontal Agents” begin to perform complex cognitive tasks, the demand for job security in the service and corporate sectors will peak.

While Ethan Choi’s analysis provides a robust framework for the “bull case” (infinite demand and massive growth), my observation (from a recent article) regarding circular financing and debt exposure is the critical “bear case” that many institutional analysts are flagging in 2026, and deserves fair focus.

Glossing Over Realities

Below is a breakdown of the points Choi arguably glosses over, which are essential to understanding the financial fragility of the current buildout.

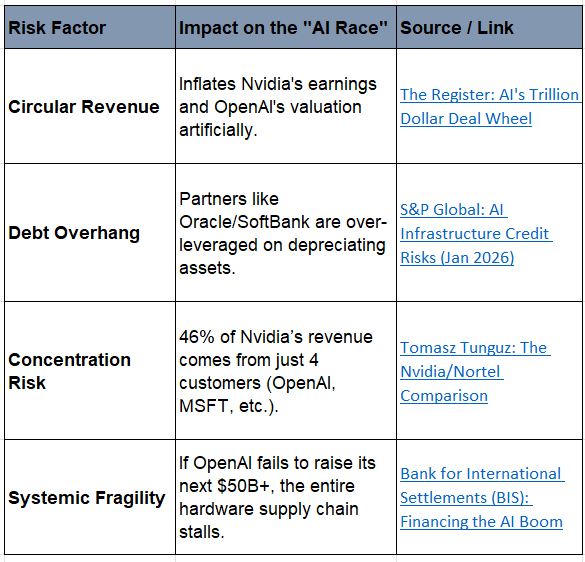

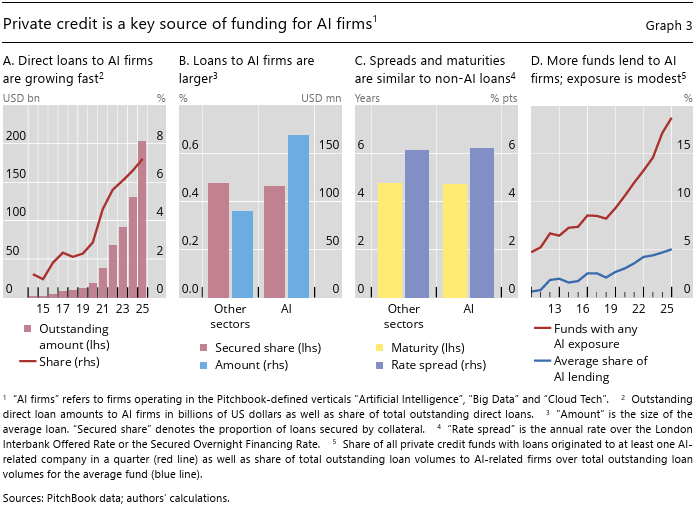

1. The “Circular Economy” of Nvidia & OpenAI

Critics argue that the $1.4T infrastructure web is not a series of independent market transactions but a closed-loop recycling scheme.

Vendor Financing: In 2025, Nvidia announced a strategic partnership to invest up to $100 billion in OpenAI over several years.

The “Round Trip”: Skeptics (including reports from The Register and Highline Wealth Partners) point out that much of the capital Nvidia “invests” in OpenAI or Anthropic is immediately returned to Nvidia to purchase Blackwell or Vera Rubin chips.

Accounting Concerns: This creates a “mirage” of high revenue growth. If Company A gives Company B money to buy Company A’s products, the “revenue” is technically real, but it doesn’t represent organic market demand—it represents subsidized demand.

Note: This mirrors the “vendor financing” crisis of the 2000 Telecom Bubble (specifically Lucent and Nortel), where equipment makers lent billions to startups to buy their gear, leading to a massive crash when the startups couldn’t pay it back.

Of course, as a separate matter, I somewhat disagree on some of the technicalities and issues of depreciation, here:

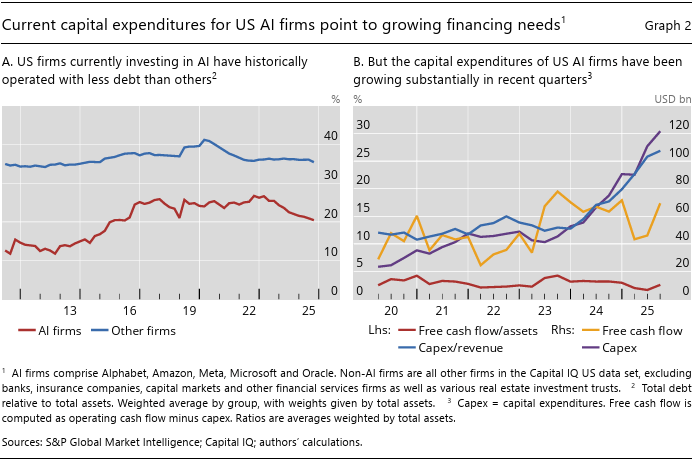

2. The “GPU-Backed Debt” Mountain

OpenAI’s partners (Oracle, SoftBank, CoreWeave) have accumulated nearly $100 billion in debt by the end of 2025 to fund these data centers.

The Collateral Problem: Much of this debt is “GPU-backed.” In 2025, CoreWeave alone secured over $10B in debt using Nvidia GPUs as collateral.

The Depreciation Risk: Unlike real estate, chips depreciate at lightning speed. If a new architecture (like the Vera Rubin) makes older Blackwell chips obsolete, the “collateral” backing billions in debt could evaporate overnight. Note: I have countered this particular argument in “Why Michael Burry Is Wrong About Depreciation”, but it deserves consideration.

Financial Stability: The Bank of England and S&P Global warned in January 2026 that the speed of this debt accumulation is “unprecedented” and could create systemic risk if AI monetization (ARR) doesn’t catch up to the cost of debt service.

3. The $600B “Revenue Gap”

Choi’s “1 GW = $10B ARR” rule assumes a linear path to monetization. However, research from David Cahn (Sequoia) and later J.P. Morgan Reports (below) highlights a massive disconnect.

The Gap: Analysts estimate that the industry needs to generate $600B more in annual revenue than it currently does just to break even on the hardware being bought today.

Negative Free Cash Flow: Despite a $20B run rate, OpenAI is projected to remain cash-flow negative until 2029 or 2030. This means they are entirely dependent on continuous “mega-rounds” of funding to service their $1.4T in commitments.

4. Summary of Risks Not in the Choi Thread

These are good reads, and will make you think twice, and thrice, and thensome, from a risk perspective:

The Register: AI’s Trillion Dollar Deal Wheel

S&P Global: Where are AI Investment Risks Hiding (Jan 2026) and AI Infrastructure Buildout Weighs Credit Risks and Rewards

Tomasz Tunguz: The Nvidia/Nortel Comparison

Bank for International Settlements (BIS): Financing the AI Boom

The “Tale of Two AIs”: While startups are scaling, big enterprises are struggling with “AI fatigue” and high implementation costs, leading to a bottleneck in actual profit realization: Sequoia Capital: AI in 2026 - A Tale of Two AIs — The updated “600 Billion Dollar Question” for the 2026 fiscal environment.

Thoughts

While Ethan Choi is right that the technical potential is infinite, the financial bridge to get there is built on a high-stakes mountain of debt and “fiscal incest.” If the “Horizontal Agent” era doesn’t start delivering actual profit (not just ARR) by 2027, the buildout Ethan describes may face a massive deleveraging event.

Indeed, demand might be infinite in the long run, but capital has a "speed limit" dictated by debt servicing and hardware depreciation, if not applied responsibly!

This video provides an excellent visual ranking of the "Giga-factories" mentioned in Ethan Choi's analysis and how they compare in scale across the global landscape.

Additional References and Considerations

The Central Debate

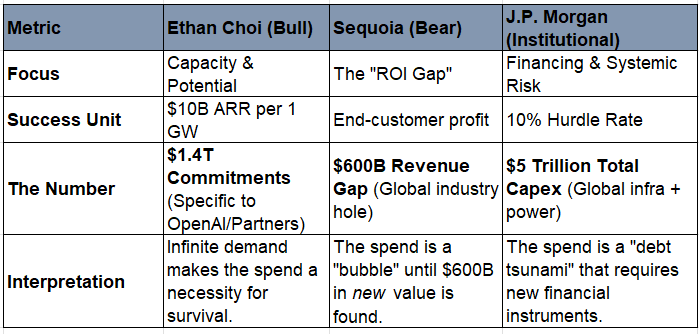

In January 2026, the comparison between Ethan Choi’s (Khosla Ventures) “Infinite Demand” framework and Sequoia Capital’s (David Cahn) “$600 Billion Question” is the central debate of the AI economy.

In a way, Ethan Choi focuses on the input (securing Gigawatts and chips to meet future demand), Sequoia focuses on the output (the revenue required to make those inputs profitable).

1. The Core Economic Clash

Sequoia’s $600B question (updated in late 2025/2026 to reflect current spending) highlights a massive “ROI Gap.”

2. How the $600 Billion Math Works in 2026

David Cahn’s original 2024 thesis has been updated by 2026 market realities (often cited as the “$650 Billion Gap” in recent J.P. Morgan and Sequoia reports).

The math is simple but brutal:

Nvidia Revenue: Projected at ~$150B–$200B in data center revenue.

Total Data Center Cost: You must double the GPU cost to account for energy, buildings, and backup power (The “2x Rule”). This puts the buildout at $300B–$400B.

End-User Margin: To give the buyers (Microsoft, OpenAI, etc.) a healthy profit, the end-user revenue must be roughly double the total cost.

The Result: The industry needs ~$600B+ in annual AI revenue to be economically sustainable.

3. Why Ethan Choi is More Optimistic

Choi’s analysis implies that we shouldn’t worry about the $600B gap because:

Marginal Cost of Intelligence: As we hit 30 GW, the cost per “unit of intelligence” drops so low that new industries (robotics, drug discovery, etc.) will emerge to fill the revenue gap.

The “Horizontal Agent” Catalyst: Sequoia’s 2024 skepticism was based on “chatbots.” Choi’s 2026 optimism is based on Agents—autonomous software that can do the work of a human employee 24/7. One “Agent” could generate 10x the revenue of a “Copilot.”

The Debate

Sequoia asks: “Is the revenue real?” (Pointing to the fact that only ~15% of enterprises see a clear EBITDA lift so far).

Choi asks: “Is the power secured?” (Pointing to the fact that those who don’t have the GWs won’t be able to compete when the “Horizontal Agent” era hits full stride).

The 2026 Consensus: We are currently in a “Stabilization Year.” The massive $1.4T infrastructure web Ethan describes is a bet that the $600B revenue gap Sequoia identified (and JP Morgan highlights as a critical consideration), will be closed by the autonomous labor market between 2027 and 2030.

You be the judge of which is which.

Notes:

The ROI Gap: While Choi is right about capacity, Sequoia is right about the current $600B+ “hole” in the balance sheet.

The Debt Warning: Also worth noting are a few of the references provided above and the several J.P. Morgan Reports that warn that if the revenue doesn’t materialize by late 2027, the “GPU-backed debt” model could face a credit crunch.

J.P. Morgan and a few of the references below highlight risks and the potential “bear case”. These directly address the gap between Choi’s optimism and the cold reality of debt:

General: J.P. Morgan 2026 Market Outlook

Outlook Report (PDF): Outlook 2026: Promise and Pressure

The U.S. Is Betting the Economy on ‘Scaling’ AI: Where Is the Intelligence When One Needs It? or Pdf

For a deeper dive into the financial risks, this interview with Sequoia’s David Cahn explains the origins and current status of the $600 billion challenge.

Sequoia’s David Cahn on the $600B Question

Takeaways from the J.P. Morgan Report, Sequoia Etc.

The $5 Trillion Bill: J.P. Morgan predicts a total of $5 trillion will be spent on AI infrastructure over the next five years.

Power as the Hard Ceiling: Reports estimates a need for 122 GW of new capacity by 2030—roughly the equivalent of dozens of nuclear plants.

The “Circular” Dependency: It explicitly warns about the “circular dependencies” in financing, where hyperscalers divert up to 70% of their operating income into CapEx to sustain the very market they are selling into.

The Historical Warning: J.P. Morgan’s biggest fear is a repeat of the Telecom Bubble (1990s), where billions were spent on fiber-optic networks that sat “dark” for a decade before becoming profitable.

The reference to the $5 trillion figure comes from a J.P. Morgan Global Research analysis released in late 2025 (titled “AI Capex – Financing the Investment Cycle” and referenced in their 2026 Outlook).

It is a cumulative projection of global investment required for data centers, power supplies, and AI hardware through 2030:

1. The $5 Trillion Math (J.P. Morgan)

J.P. Morgan estimates that building out the global data center and AI infrastructure to meet projected demand will cost over $5 trillion in total capital expenditure over the next five to seven years.

The Revenue Requirement: To achieve a modest 10% return (IRR) on this $5 trillion spend, the industry would need to generate approximately $650 billion in annual revenue in perpetuity.

The “iPhone Index”: To put this in perspective, J.P. Morgan noted that this revenue would be the equivalent of every current iPhone user in the world paying an additional $35 per month for AI services.

2. Comparison: Choi vs. Sequoia vs. J.P. Morgan

These three frameworks represent the “Bull,” “Bear,” and “Institutional” views of the same $1.4T to $5T buildout.

Link:

Techstrong reference article to JPMorgan’s numbers

4. The Disconnect

I guess the reason Ethan Choi doesn’t focus on the $5T is that he views it as “The Price of Admission.” In his framework, if you don’t spend it, you don’t get the Gigawatts. J.P. Morgan, and many others, however, view it as a “Credit Risk,” noting that traditional hyperscaler cash flow ($700B/year) won’t be enough to cover a $5T buildout, necessitating the leveraged finance and securitization (GPU-backed debt) identified as a risk.

Reference:

Edward Conard: “AI Capex – Financing the Investment Cycle,” Nov 10, 2025.

J.P. Morgan Wealth Management: “Outlook 2026: Promise and Pressure,”.

J.P. Morgan 2026 Outlook: AI Lift and Economic Drift