Infrastructure Evolution: Why It Didn't Matter Then vs Why IaaS Companies Have the Edge Now

A Path With Many Twists & Turns

I have a theory. And only time will allow us to see how this plays out. Yes, only time will tell. Consider it a (couple of) Counter-point(s).

Perhaps because we have never experienced this monumental shift, presently playing out, right in front of us, that its future is not only “jagged”, but will become “a path with many twists & turns”, so to speak - triggered by the tremendous focus or drive towards “AGI”? “ASI”? Terms of which I have never been too hung up about, but see tremendous potential in, towards (better) future possibilities.

This are my thoughts on Grace Shao's briliantly thought through, presented and I must admit, already on its solid trajectories, but for which, i think may take a slightly different “right-turn”: “China's AI Boom Could Be The Catalyst For Its Cloud Boom.” My add on: Driven By Infrastructure.

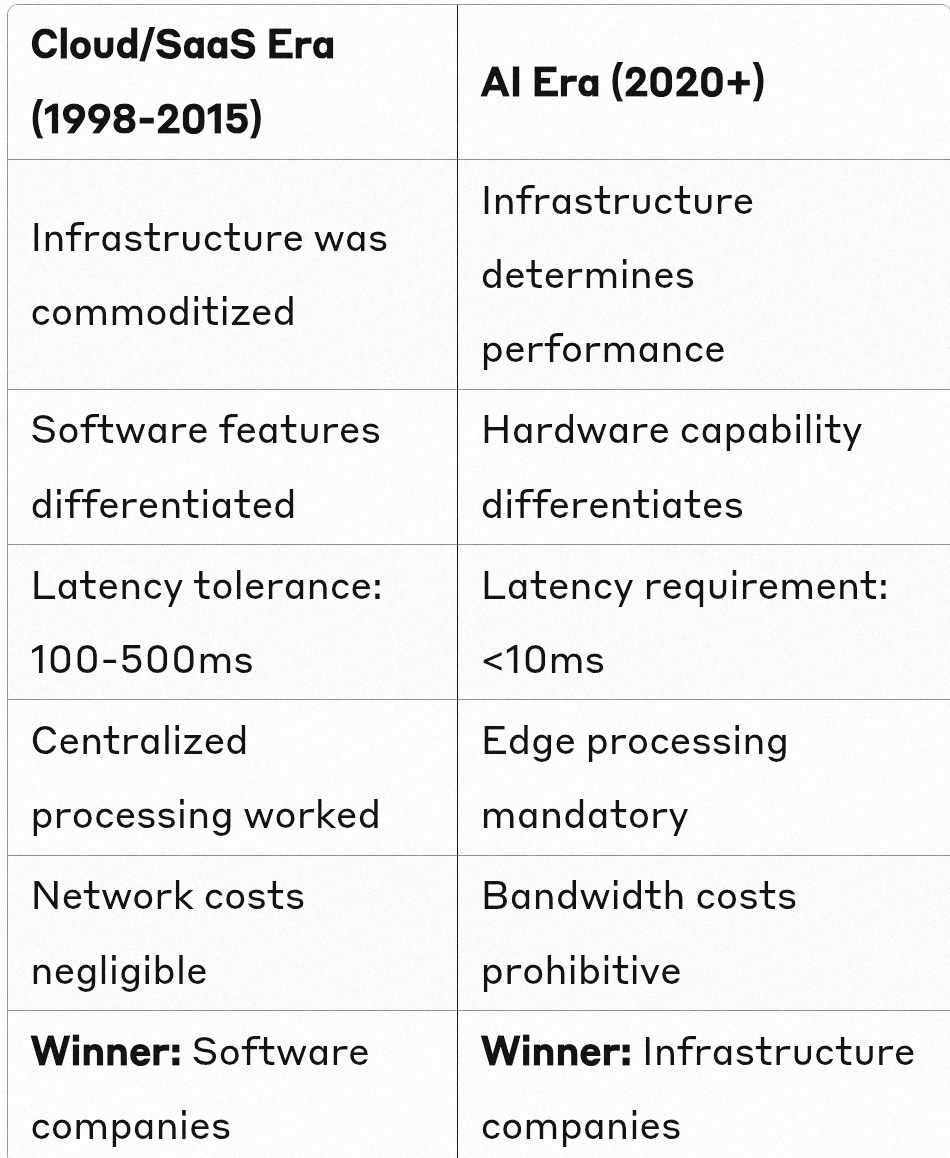

Part 1: Why Infrastructure Didn't Matter in the Cloud/SaaS Era (1998-2015)

The Technology Context

Basic Computing Was Sufficient

Web applications required simple server processing

Standard x86 servers could handle business logic

Network bandwidth needs were minimal (text/basic web pages)

Latency tolerance was high: 100-500ms delays were acceptable for web apps

Company Evolution Examples

1. NetSuite vs Traditional ERP (1998-2016)

NetSuite's Winning Strategy:

Founded in 1998, became the first cloud computing software company

Competed against Oracle's on-premises ERP systems

Won through software differentiation, not infrastructure:

Unified business platform vs fragmented Oracle modules

No IT management required vs expensive Oracle infrastructure teams

Subscription model vs massive upfront Oracle licensing costs

Why Infrastructure Didn't Matter:

Both NetSuite and Oracle could run on commodity servers

Network requirements were minimal (business data entry/reporting)

Oracle's superior data centers provided no competitive advantage

NetSuite eventually ran on Oracle's infrastructure after acquisition

2. Salesforce vs Traditional CRM (1999-2010)

Salesforce's Path to Victory:

Launched 1999, reached $1 billion revenue by 2009

Defeated Siebel, Oracle CRM, and Microsoft CRM

Won through user experience and business model innovation:

Browser-based vs desktop installation

Pay-per-user vs expensive site licenses

Continuous updates vs infrequent software releases

Mobile accessibility vs desktop-only systems

Infrastructure Was Commoditized:

CRM applications had low computational requirements

Basic web servers could handle sales data processing

Competitors like Oracle had better data centers but lost anyway

Network latency didn't impact sales workflow productivity

Step-by-Step: Why Software Beat Infrastructure (2000s-2010s)

1. Application Requirements Were Simple

↓

2. Commodity Hardware Was Sufficient

↓

3. Infrastructure Became a Cost Center

↓

4. Software Features Became the Differentiator

↓

5. User Experience Determined Market Winners

Key Insight: In this era, having better servers, networks, or data centers provided no competitive advantage because the applications didn't stress these resources.

Part 2: Why Infrastructure Companies Have the Edge in the AI Era (2020+)

The Technology Context Has Fundamentally Changed

AI Demands Extreme Performance

Real-time AI inference requires specialized hardware (GPUs, TPUs)

Latency requirements dropped from 500ms to <10ms for critical applications

Bandwidth costs exploded due to video/sensor data processing

Edge processing became mandatory for privacy and performance

Step-by-Step: Why Infrastructure Now Determines AI Success

Step 1: Latency Requirements Became Extreme

Autonomous Vehicles Example:

Traditional web app: 500ms delay = slight user annoyance

Autonomous vehicle AI: 500ms delay = fatal accident

Solution: Edge AI reduces delay to "only a few milliseconds, enabling the car to react within centimeters at maximum vehicle speeds"

Step 2: Hardware Specialization Became Critical

AI Processing Requirements:

Traditional apps: Standard CPUs sufficient

AI applications: "Currently, most existing onboard AI computing tasks for autonomous vehicle applications including object detection, segmentation, road surface tracking, sign and signal recognition are mainly relying on general-purpose hardware – CPUs, GPUs, FPGAs"

Key difference: Infrastructure performance directly determines AI capability

Step 3: Edge Processing Became Mandatory

Why Centralized Cloud Fails for AI:

"Edge computing relieves the real-time requirements that cloud computing cannot meet in some scenarios"

"Edge AI refers to AI algorithms deployed on edge devices for local processing, which can process data without a network connection"

Result: Proximity to users (infrastructure advantage) became decisive

IaaS Companies' Specific Advantages in AI Era

1. Physical Infrastructure Control

Telecom Infrastructure Companies (China Mobile, Verizon, etc.):

Own Cell Towers → Own Fiber Networks → Own Edge Locations

↓ ↓ ↓

Low Latency + High Bandwidth + Physical Proximity

↓ ↓ ↓

= Optimal AI Performance

Competitive Advantage:

Google Edge TPU example: "A dedicated hardware accelerator designed to perform high-speed machine learning (ML) inference on edge devices"

Infrastructure companies can deploy these at scale across their existing network

2. Cost Structure Advantages

Traditional Cloud Economics (Broken by AI):

User Data → Internet → Cloud Data Center → AI Processing → Results Back

↑ ↑ ↑ ↑

Expensive Latency Limited Capacity More Latency

Infrastructure Company Economics (AI-Optimized):

User Data → Local Edge AI Processing → Immediate Results

↑ ↑ ↑

Minimal Cost No Latency Real-time Response

3. Hardware Integration Control

Traditional Software Companies' Limitation:

Must rely on third-party infrastructure

Cannot optimize hardware-software stack

Limited control over performance bottlenecks

Infrastructure Companies' Advantage:

Full stack control from network protocols to AI accelerators

Can optimize entire pipeline for AI workloads

Direct hardware-software co-design capability

Real Company Evolution Examples

China Mobile's AI Transformation (2020+)

Strategic Evolution:

2020: Basic telecom services + commodity cloud infrastructure

2022: Edge computing pilots with AI inference capabilities

2024: Full-scale AI edge deployment leveraging 5G network. https://www.rcrwireless.com/20250627/5g/china-5g-base-stations

2025+: AI-first infrastructure company competing directly with Alibaba Cloud

Competitive Advantage:

Existing relationships with Chinese enterprises

Physical infrastructure already deployed nationwide

Lower cost structure than pure-cloud competitors

Regulatory advantages as SOE in Chinese market

Verizon's AI Edge Strategy

Evolution Path:

Traditional Era: Just a "dumb pipe" for internet connectivity

Cloud Era: Infrastructure partner for AWS/Azure

AI Era: Direct competitor offering edge AI services

Current: "5G Edge with AWS" combining Verizon's network + AI processing

Key Insight: Verizon went from infrastructure commodity to AI differentiator by leveraging physical proximity

Part 3: Why This Time is Different - The Reversal

The Fundamental Shift

The Competitive Reversal

Then: Oracle (infrastructure leader) lost to Salesforce (software innovator) Now: Alibaba Cloud (software leader) faces threat from China Mobile (infrastructure owner)

Why the reversal happened:

Performance Requirements Changed: AI applications stress infrastructure in ways web apps never did

Physics Became Limiting: Speed of light creates unavoidable latency in centralized systems

Economics Inverted: Bandwidth costs for AI workloads make edge processing economically necessary

Specialization Required: Generic cloud infrastructure insufficient for AI-specific hardware needs

Implications for China's Market

Original Thesis: "SOE players China Mobile and China Telecom might not be able to offer competitive service in PaaS + SaaS layers"

Reality: Companies like Huawei, China Mobile and China Telecom are advantaged because:

They control the physical infrastructure that determines AI performance

They have existing enterprise relationships and SOE status advantages

They can offer end-to-end solutions from network to AI services

They have lower cost structures than pure-cloud competitors

Edge AI favors their distributed physical infrastructure

Part 4: Current Acceleration - Infrastructure Companies' AI Edge Push (2024-2025)

Verizon's Aggressive AI Transformation

Major Strategic Shift (2024-2025):

January 2025: Verizon Business launches AI Connect, providing low-latency edge computing for AI workloads, meeting the surge in real-time, with partnerships including Google Cloud, Meta, NVIDIA, and Vultr

December 2024: Verizon engineers will begin demonstrations of this solution in early 2025 with NVIDIA for AI workloads on 5G private networks

Strategic Partnerships: Verizon's AI Connect partners and customers include hyperscalers such as Google Cloud and Meta, which are tapping Verizon's network infrastructure for their AI workloads. Chipmaker giant Nvidia and GPU-as-a-service company Vultr are looking to Verizon to integrate their GPUs into Verizon's infrastructure

Market Opportunity Recognition: The AI edge computing sector is forecast to expand tenfold from $27 billion in 2024 to $270 billion by 2032. Delivering AI to the edge is key to facilitating the growth of self-driving cars, robotics, and the Internet of Things

China Mobile's AI-First Strategy

Enterprise AI Integration (2024):

China Mobile has enhanced its "people-car-home" service offerings and formed channel partnerships with 10 top-tier automakers. The company is also involved in pilot projects for "vehicle-road-cloud integration" in various cities, further advancing its IoV services

China Unicom's Acceleration (2025):

Beijing-based China Unicom, whose main businesses include mobile and broadband networks and cloud and data centres, saw its profit grow 10.1 per cent year on year in 2024. Cloud revenue rose by 17.1 per cent, driven by strong growth in its intelligent computing sector

Huawei's Full-Stack AI Investment

Strategic Commitment (2024-2029):

In 2024 and over the next five years, Huawei will invest even more into ecosystem development in an effort to guide and drive broader development in the computing and device industries. Their goal is to offer the world a second option for computing, and a third option for mobile OS

AI-Native Cloud Strategy (2025):

Today, AI is changing everything. Countries and companies are putting AI as a core strategy, and have the chance to build their own models. AI is not a game of heavy costs. AI models can be optimized by leveraging the achievements from the open source community

Market Context: Explosive Growth

Edge Computing Market Expansion:

The global edge computing market size was estimated at USD 23.65 billion in 2024 and is expected to reach USD 327.79 billion in 2033, growing at a CAGR of 33.0% from 2025 to 2033

China's Edge AI Leadership:

The edge AI market in China is experiencing robust growth, driven by significant investments in artificial intelligence and a rapidly expanding consumer electronics sector. Chinese tech giants like Huawei and Baidu are leading the development of edge AI applications, particularly in smart cities

Comparison: Pre-AI Era vs AI Era Investment Patterns

Pre-AI Era (2010-2020): Minimal Edge Investment

Telecoms focused on basic connectivity and infrastructure partnerships

Edge computing was experimental, limited to CDN optimization

No significant AI-specific hardware investments

Revenue models remained traditional (connectivity + basic cloud partnerships)

AI Era (2024-2025): Massive Edge AI Investment

Verizon: Complete AI strategy overhaul with dedicated AI Connect platform

China Mobile/Unicom: Double-digit cloud revenue growth driven by AI computing

Huawei: Five-year commitment to ecosystem development for computing alternatives

Industry-wide: Partnerships between AI hardware firms and telecom operators accelerated the deployment of 5G-enabled edge AI solutions

Key Acceleration Indicators

Partnership Strategy Changed: From basic infrastructure partnerships to co-developing AI solutions with NVIDIA, Google Cloud, Meta

Revenue Model Shifted: From connectivity fees to AI workload monetization

Investment Focus: Hardware integration for AI-specific requirements vs generic cloud capacity

Customer Relationships: Direct enterprise AI services vs just providing network access

Part 5: New Infrastructure Entrants - The Game Has Completely Changed

Massive New Capital Deployments

The Stargate Project: $500B Infrastructure Commitment (2025)

Unprecedented Scale: The Stargate Project is a new company which intends to invest $500 billion over the next four years building new AI infrastructure for OpenAI in the United States. We will begin deploying $100 billion immediately

Strategic Partners: "The Stargate Project is a new company which intends to [build] new AI infrastructure for OpenAI in the United States," OpenAI, Oracle, and SoftBank said in a joint statement

Scale Beyond Traditional Cloud: We now expect to exceed our initial commitment thanks to strong momentum with partners - Oracle and SoftBank are betting their future on AI infrastructure, not traditional cloud services.

xAI's Colossus: The Tesla-AI Infrastructure Convergence

Massive GPU Deployment: xAI's "Colossus" runs on 200,000 Nvidia H100 GPUs synced by high-speed interconnects. Igor Babuschkin calls it "the biggest, fully connected H100 cluster of its kind."

Expansion Strategy: In November 2024, xAI announced it would double the capacity of Colossus through a multibillion-dollar deal. The firm plans to raise $6 billion in the coming years, with the bulk of it coming from Middle Eastern sovereign wealth funds. It will cover the cost of adding 100,000 more GPUs

Tesla Integration: xAI is bolstering its Colossus 2 data center in Memphis with 168 Tesla Megapacks, enhancing the energy infrastructure for its ambitious AI supercomputer expansion

ROI Extraction Through Vertical Integration

xAI → Tesla L4 Autonomous Driving Pipeline

Strategic Vision: Elon Musk is currently seeking approval from Tesla's board for a $5 billion investment in xAI. xAI utilizes data centers to provide the computational power and storage necessary for training and running its AI chatbot, Grok. https://edition.cnn.com/2025/07/14/tech/tesla-musk-shareholder-vote-xai

Performance Advantage: Each H100 packs 80 GB of HBM2e memory at 2 TB/s bandwidth and nearly 4 PFLOPS of FP8 performance with sparsity - this level of computational power will enable real-time vehicle intelligence that competitors cannot match.

Market Differentiation: Grok 4 is (based on benchmarks) one of the most intelligent model in the world. It includes native tool use and real-time search integration - if integrated with Tesla's autonomous driving, this creates an unassailable competitive moat.

Geopolitical Infrastructure Fragmentation

Huawei's Forced Vertical Integration Strategy

Strategic Necessity: Cut off from Western cloud services and chip supplies, Huawei must control the full stack from chips to applications to compete globally.

Advantage Through Constraints: This forced vertical integration positions Huawei to extract maximum value from PaaS/SaaS services because they control every layer of optimization.

Market Opportunity: Serving the global south and Chinese domestic market with a complete alternative to Western AI infrastructure stack.

Why Custom Infrastructure Now Dominates

Hardware Specialization Requirements

Beyond Generic Cloud: The system will feature Tesla Megapacks for power storage and advanced cooling infrastructure to handle the immense energy and thermal demands - AI workloads require purpose-built infrastructure, not commodity cloud services.

Interconnect Criticality: 200,000 Nvidia H100 GPUs synced by high-speed interconnects - latency between GPUs determines model performance, requiring custom networking solutions.

Investment Scale: xAI invests $40B in Memphis site, plans solar farm & sustainable cooling tower - the infrastructure investment dwarfs traditional software development costs.

Market Structure Transformation

From Software-First to Infrastructure-First

Traditional Cloud Era (2010-2020):

Software Innovation → Market Success → Infrastructure Follows

AI Era (2024+):

Infrastructure Control → AI Performance → Market Dominance

New Competitive Dynamics

Oracle's Transformation:

Then: Lost to Salesforce despite superior infrastructure

Now: $500B bet on AI infrastructure through Stargate project

Strategy: Control the infrastructure that determines AI performance

SoftBank's Strategy:

Vision Fund pivot: From software investing to infrastructure ownership

Long-term ROI: Extract value through controlling AI computational resources

Market position: Infrastructure scarcity drives pricing power

Key Insight: Infrastructure Scarcity Creates Value

GPU Constraint Reality:

Packing 200,000 NVIDIA H100 GPUs, XAI's infrastructure surpasses competitors like OpenAI, ascending to the top at Chatbot Arena

Limited GPU supply means infrastructure ownership = competitive advantage

Unlike software (infinitely scalable), AI infrastructure has physical constraints

ROI Through Performance:

Better infrastructure → Better AI models → Higher market value

Tesla's potential L4 autonomy depends on xAI's computational advantage

Infrastructure owners can monetize through performance differentiation

Conclusion: The Infrastructure Arms Race

This Time Really Is Different:

Capital Requirements: $500B investments vs traditional cloud's incremental expansion

Performance Dependency: AI model quality directly correlates with infrastructure capability

Vertical Integration Necessity: Control entire stack to optimize for AI workloads

Geopolitical Fragmentation: Infrastructure becomes strategic national asset

Scarcity Economics: Limited GPU/compute supply creates pricing power

For China Mobile, Huawei, and other infrastructure players: This represents the greatest opportunity reversal in computing history. The same infrastructure assets that were commoditized during the cloud/SaaS era have become the primary determinant of AI market success.

The Original Thesis On A Different Path: Infrastructure companies aren't disadvantaged in the AI era—they're the only companies positioned to control the resources that determine AI performance and market success.

Apologies, forgot the link, which i will include directly into the article later today due to travel. I appreciated the read a lot, with very kind thanjs: https://open.substack.com/pub/aiproem/p/chinas-ai-boom-could-be-the-catalyst?utm_source=share&utm_medium=android&r=223m94