The Dragon's Dominion: How China Conquered the Seas and What America Might Do, Strategically - The Trillion $ Opportunities

A Look at a Comprehensive U.S. Strategy for Maritime Resilience and Competitive Advantage, with Allies. A Maritime Action Plan (MAP) 2.0 or Revitalization Strategy RoadMap

The Strategic Imperative in the Maritime Domain

The world's oceans are the arteries of global commerce and the stage for geopolitical influence. The maritime ecosystem – encompassing shipbuilding, international shipping, port operations, logistics networks, financing mechanisms, and the production of specialized components – is a cornerstone of economic prosperity and a critical element of national security for any major power. Control over this complex system translates into control over trade flows, supply chain resilience, and the ability to project power globally. In a tariff-infused world, an understanding of how this side of the globe operates is critical.

Yet, the current state of this vital domain presents a stark and concerning imbalance. Over the past three decades or so, the People's Republic of China has executed a remarkably successful, state-directed strategy to achieve overwhelming dominance across nearly every facet of the maritime value chain. I say this almost with envy. It is not easy to apply any Strategy & then scale it - towards dominance! Not in a complex world, with ever-changing variables. And to grow and maintain the momentum over decades? Wow! But dominance can appear to be a threat to some.

This is a 2-part Article. Part 2 follows with Turning The Tide: What Strategy To Rebuild America’s Shipping Might?

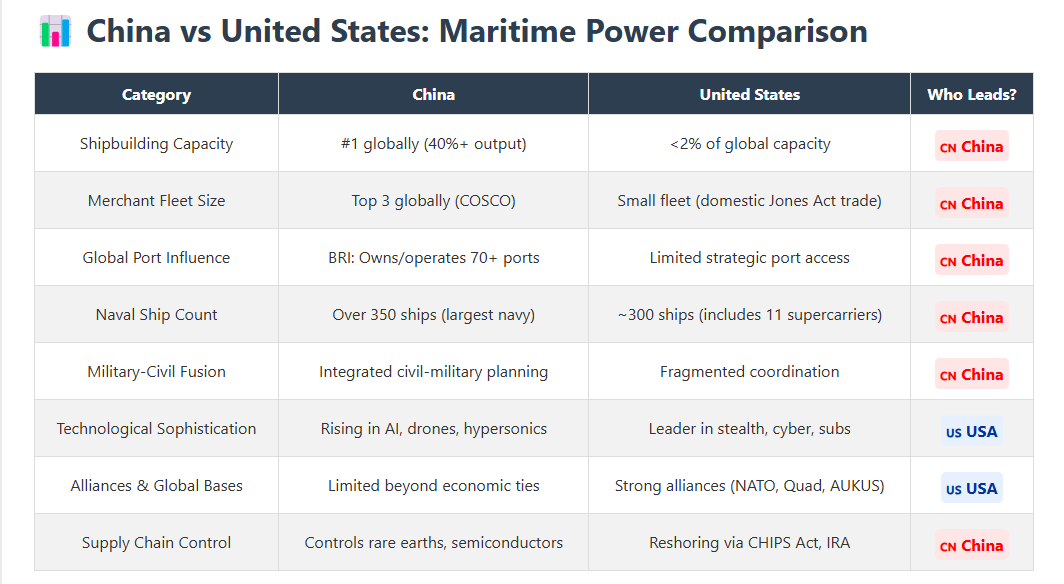

Once a peripheral player, China now commands over 50% of the global shipbuilding market by tonnage, dwarfing the United States' share, which has dwindled to less than 0.2%. China State Shipbuilding Corporation (CSSC), its state-owned champion, built more commercial tonnage in 2024 alone than the entire U.S. shipbuilding industry has since the end of World War II.

This dominance extends far beyond constructing hulls. China is the world's largest shipowning nation, controls a vast and growing network of global ports through its Belt and Road Initiative (BRI), operates the dominant state-sponsored global logistics data platform (LOGINK), and manufactures the vast majority of essential maritime equipment, including over 95% of shipping containers, 86% of intermodal chassis, and approximately 80% of the ship-to-shore cranes used even in U.S. ports.

In stark contrast, once a global leader, the United States’ maritime industrial base is fragmented and significantly diminished. Its commercial shipbuilding capacity for large ocean-going vessels is nearly non-existent, its naval shipyards face critical delays and workforce shortages, and its supply chains rely heavily on foreign, often Chinese, sources for essential components and materials.

This quick review dissects the anatomy of China's maritime ascent. It analyzes Beijing's holistic, integrated strategy—meticulously combining industrial policy, massive state financial intervention, commercial leveraging, targeted technology acquisition (particularly for complex vessels like LNG carriers and FPSOs), control over raw materials and components, specific labor dynamics, and an explicit Military-Civil Fusion (MCF) doctrine. Understanding how China built this dominant ecosystem is crucial for potentially developing a realistic and effective strategy for the United States.

Rebuilding America's maritime power cannot be a simple return to the past or an attempt to match China's scale tonnage-for-tonnage. Instead, it requires a comprehensive, sustained, and strategically focused national commitment on a bipartisan basis. This strategy must address specific U.S. competency gaps in high-value shipbuilding, critical component supply chains, competitive financing, and specialized workforce skills.

It may actively counter China's non-market practices, forge robust alliances to create resilient alternative networks ("friendshoring"), and prioritize national security resilience and technological leadership in strategic niche areas. Note that this analysis provides one possible blueprint for such an endeavor, charting a course for American maritime revitalization in the face of the dragon's formidable wake.

Note: I have a general belief system that incorporates the concept of competition as being healthy, allowing for innovation to thrive, especially given constraints. I have approached what you see below from a business perspective, wondering about how any potential player approaches a market when one dominant force already prevails. Consider it a business case study. A history lesson, maybe. Looked at in the Shipbuilding context, but could quite easily apply to anything. Consolidating a fragmented industry is many times considered a great business opportunity, but dismantling any industry already dominated by one or few players - tough. Unless there is planning. Strategy. And teamwork (otherwise known as Allies).

The $Trillion Business Case You May Ask? Well, I haven’t even considered the Commercial & Support Opportunities!

Purely from a military perspective, the Congressional Budget Office (CBO) has analyzed the U.S. Navy’s 2025 shipbuilding plan, estimating that total costs—including shipbuilding, operations, maintenance, aircraft procurement, and Marine Corps funding—will rise from $255 billion annually today to $340 billion by 2054.

If we extrapolate this over 30 years, the total spending could exceed $10.2 trillion, though exact figures depend on inflation, strategic adjustments, and unforeseen costs. The Navy plans to expand its fleet from 295 battle force ships today to 390 by 2054, requiring significant investment in shipbuilding and infrastructure - these numbers should be interesting enough to make a good business case, if it is also “handled with due care”.

But the opportunities are not limited to a military one - one huge area not yet quantified - the commercial (and support services) side of shipbuilding need to be considered also! But I am getting ahead of myself. So let’s start with a quick value chain look.

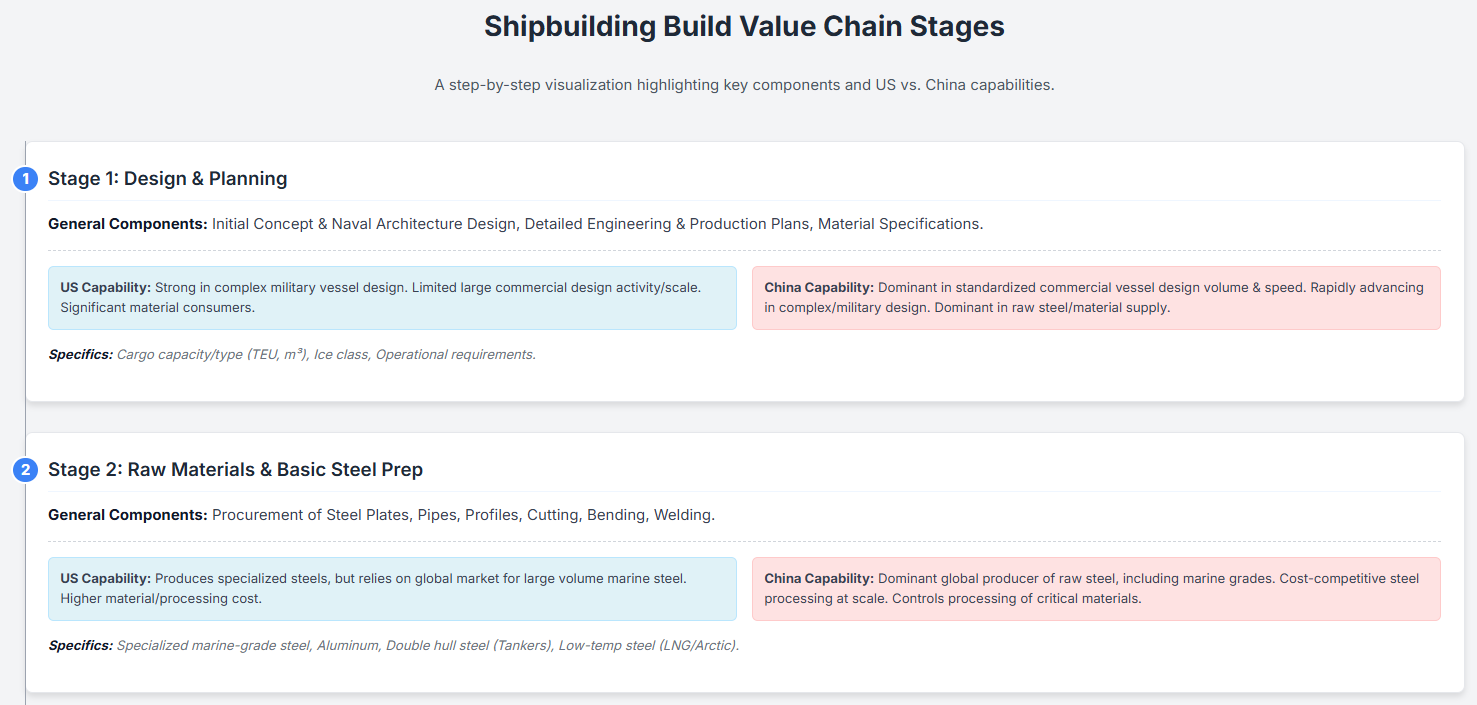

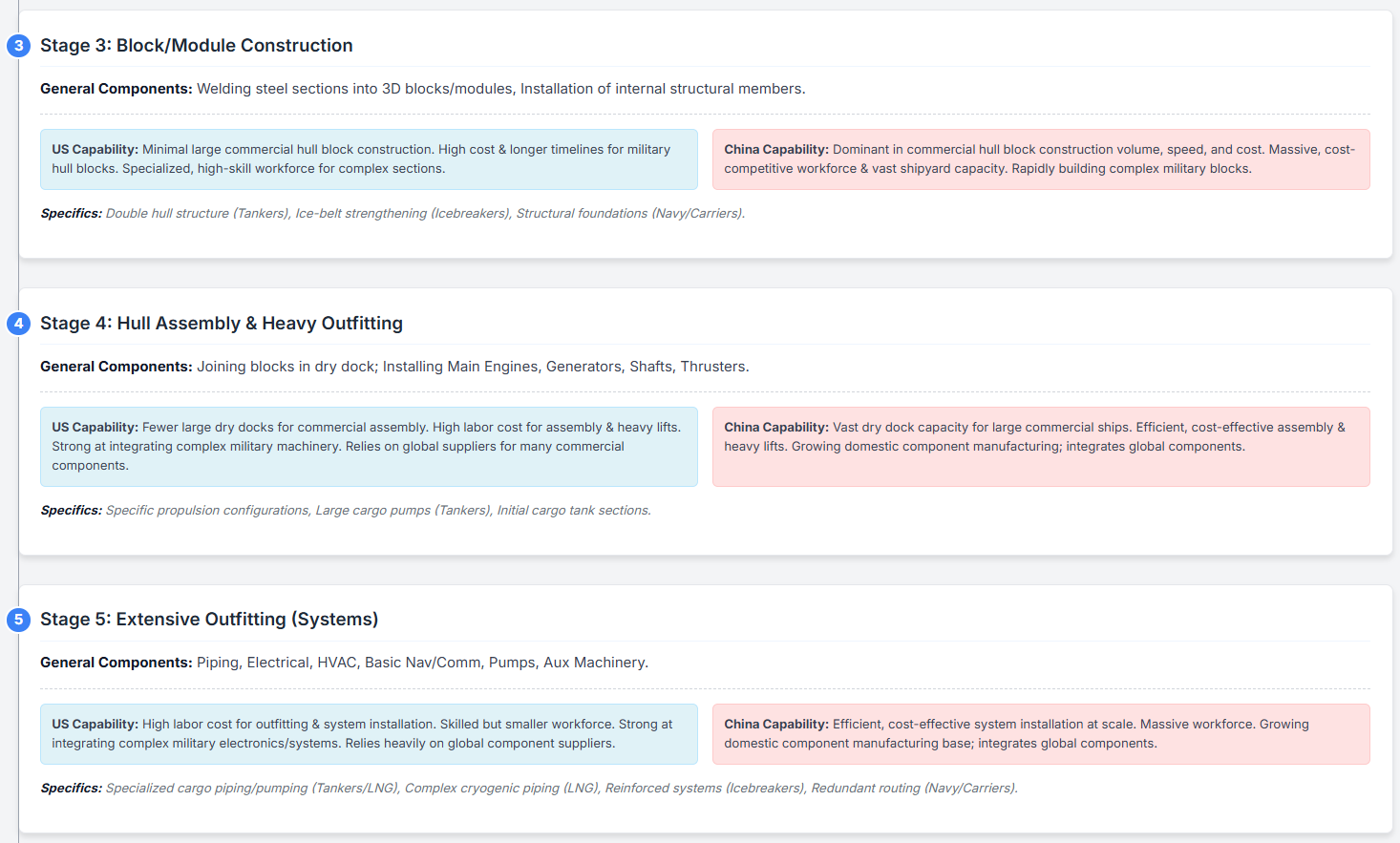

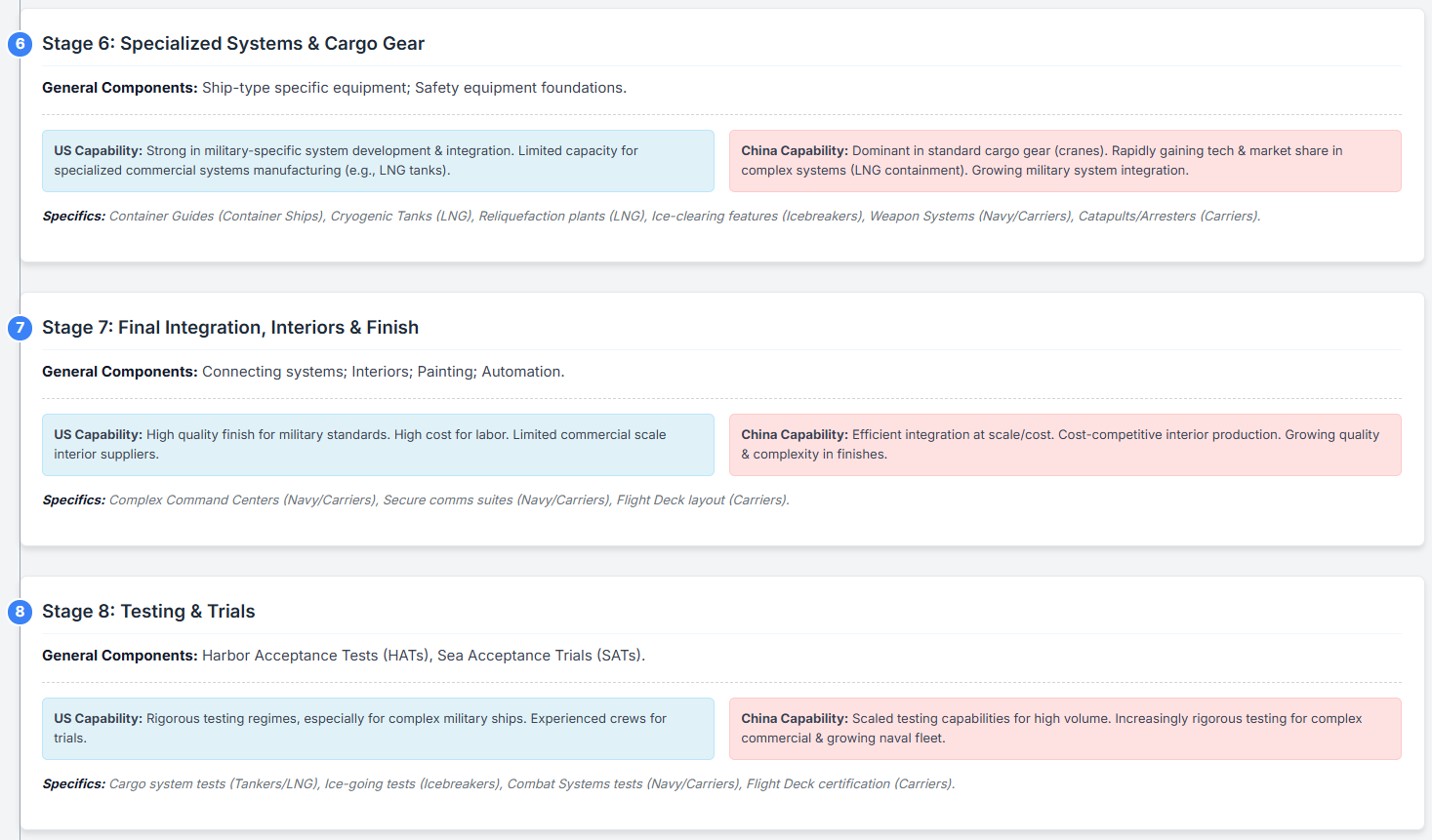

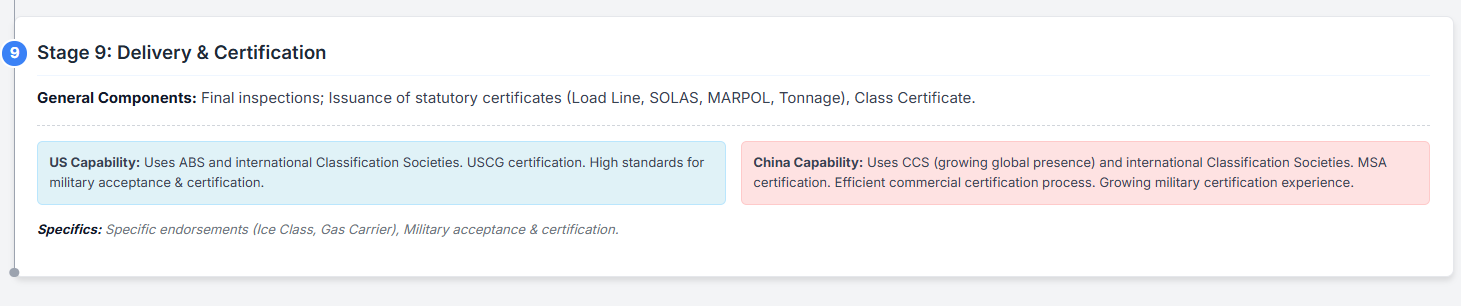

Shipbuilding Build Value Chain

What does the typical value chain look like? Well, approximately as follows. It is important to operators, builders, and financiers when looking at any one given marine construction project, to consider the following. A contrast between capabilities is also generalized below:

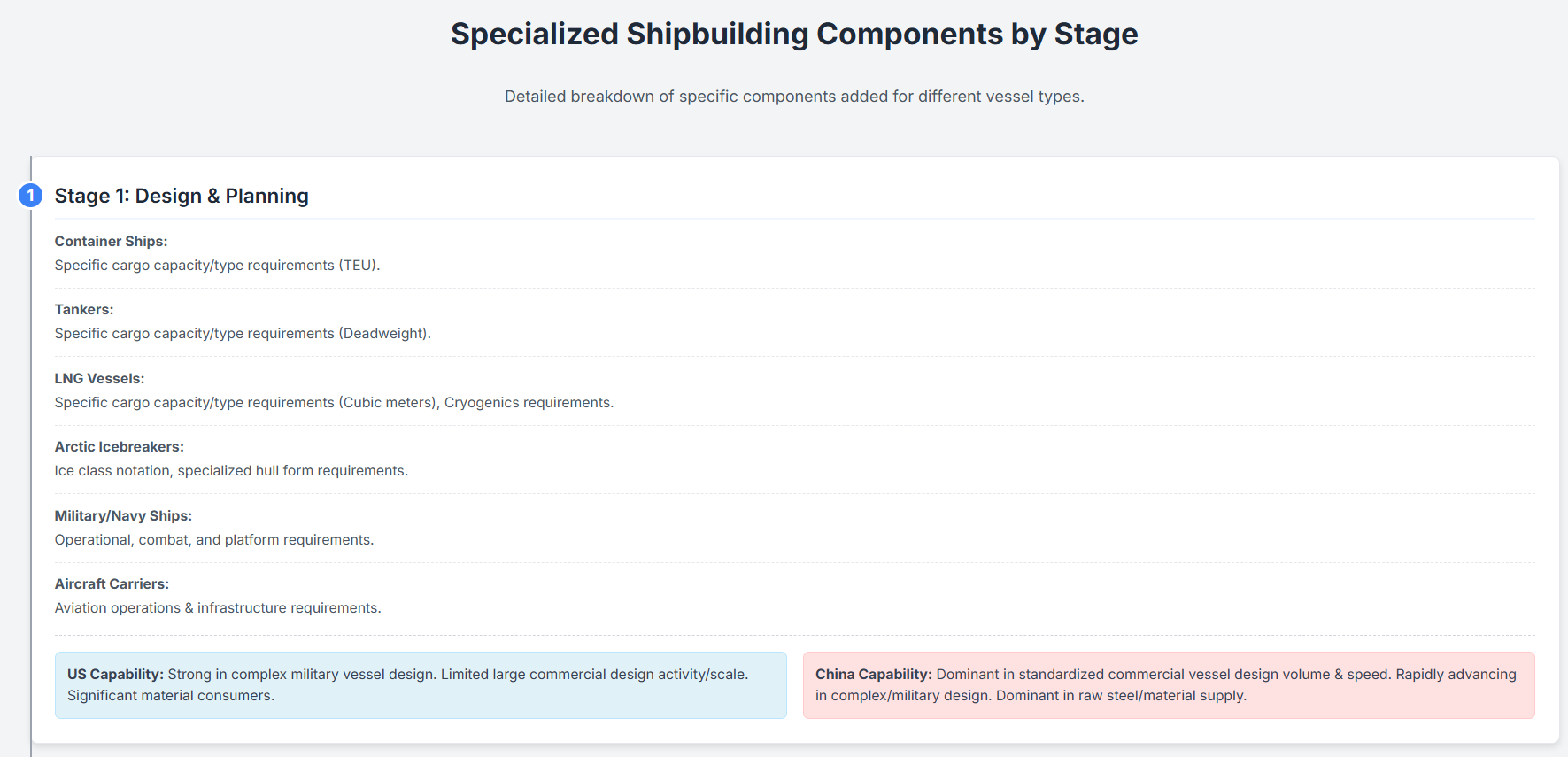

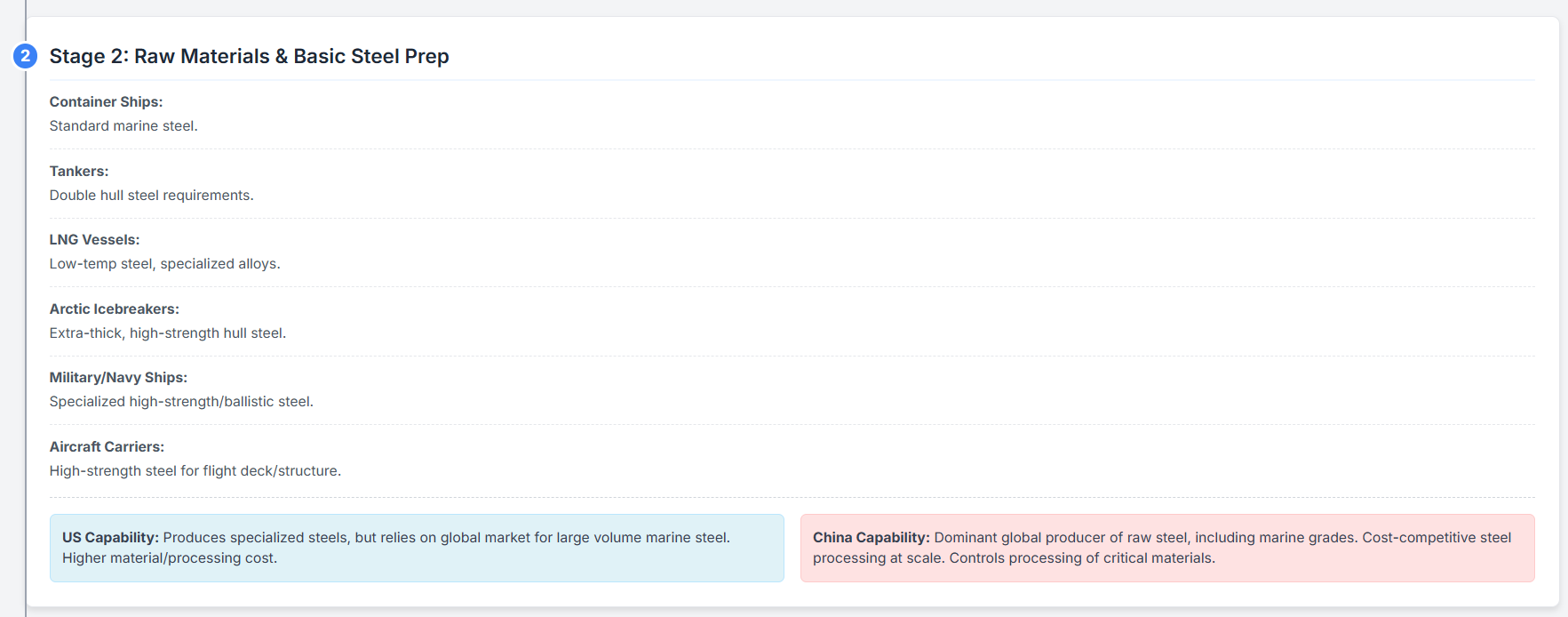

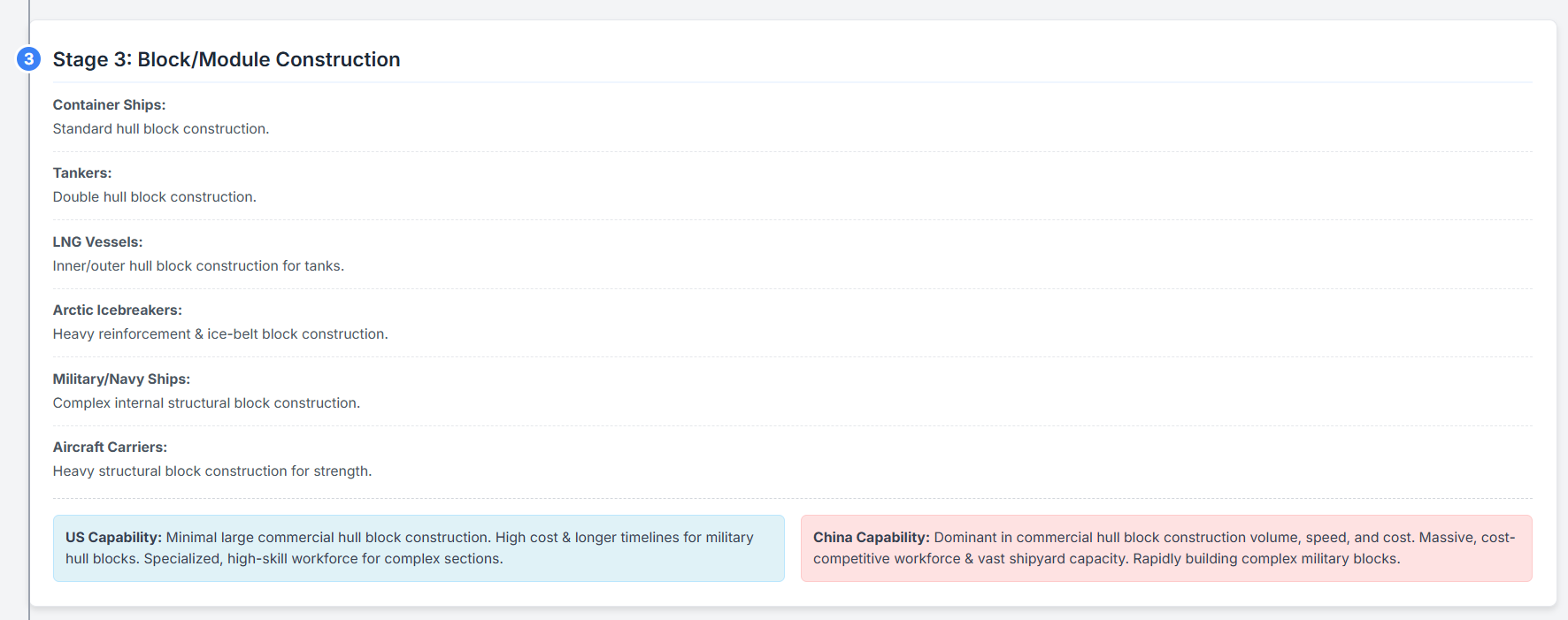

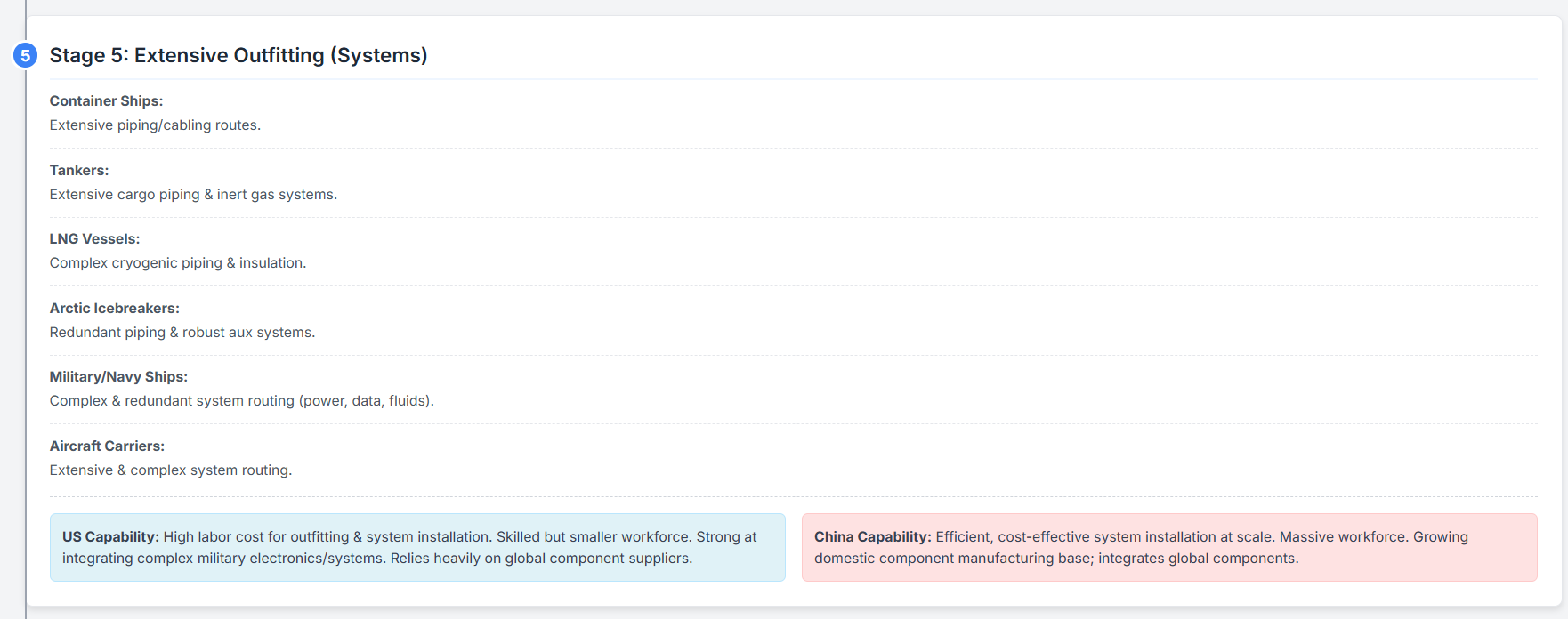

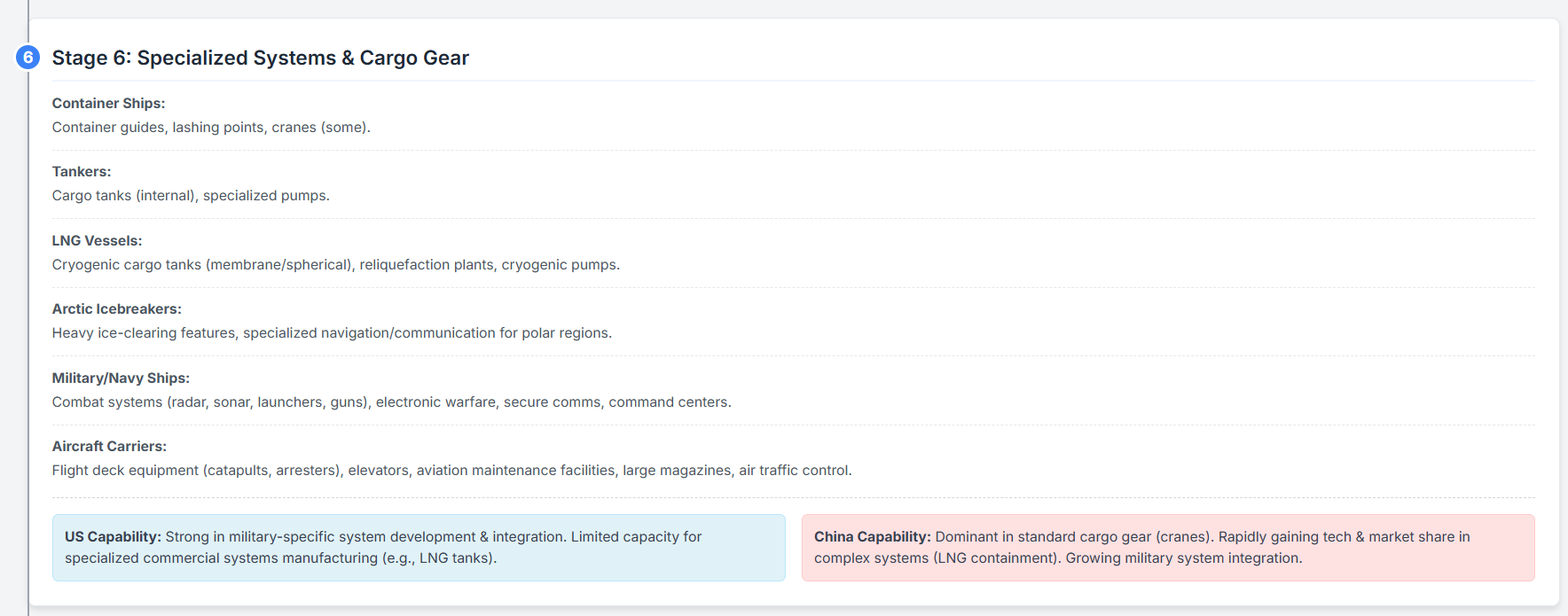

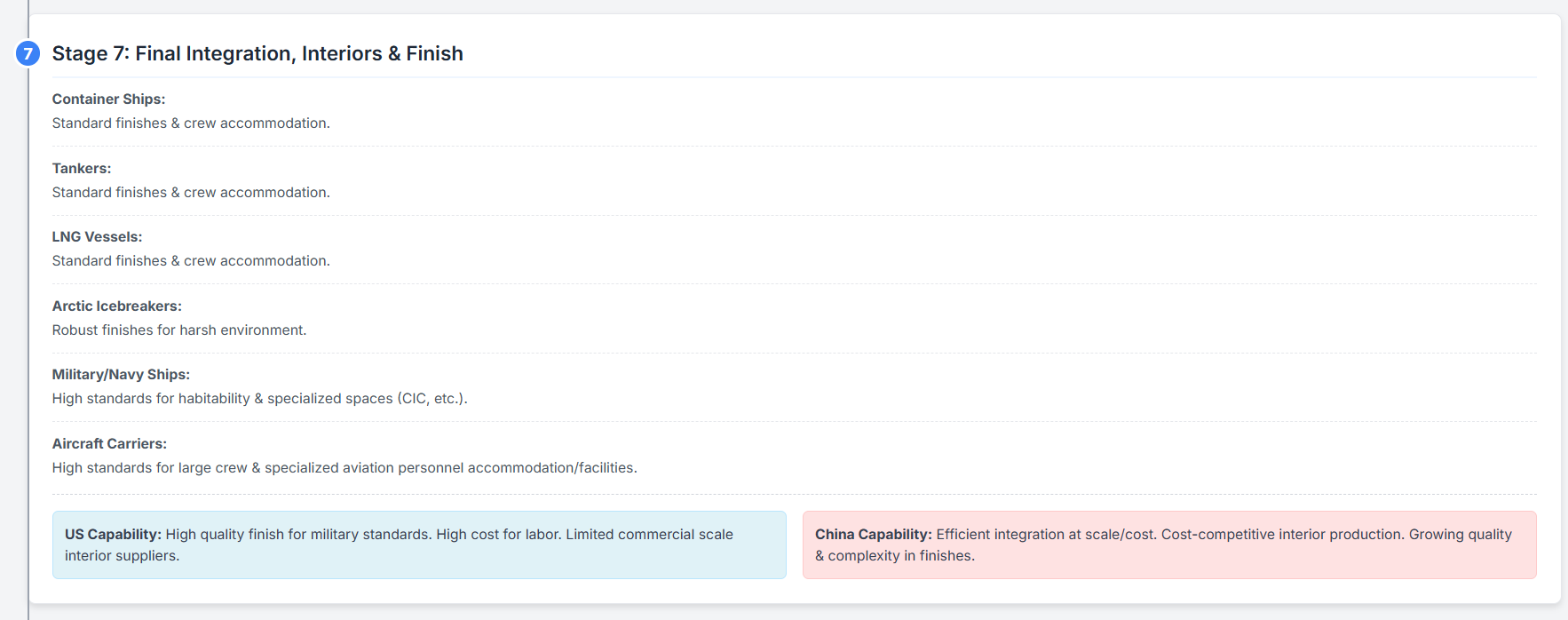

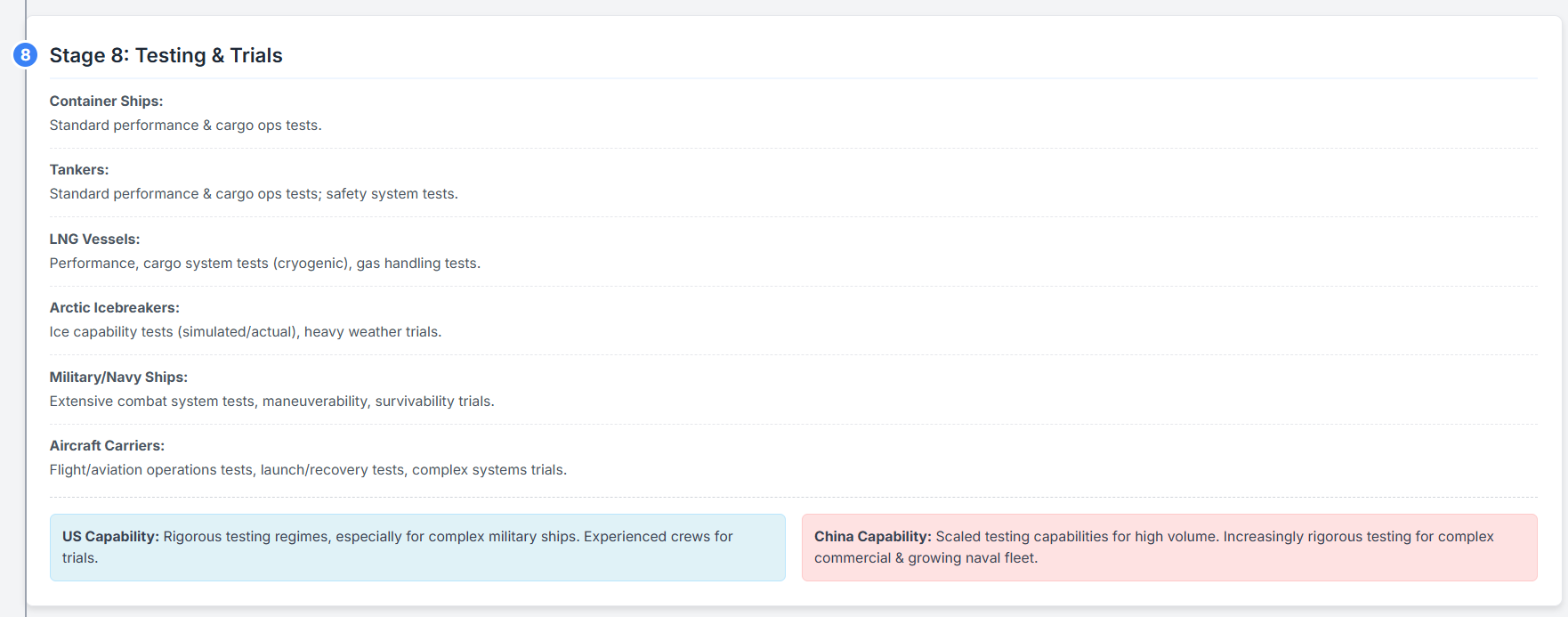

Specialized Vessels Build Stage Requirements

But not all “ships” are created equal. There are unique features to note with Container Ships, Tankers, LNG Vessels, Artic Icebreakers, Military/Navy Ships, Aircraft Carriers. A few include the following (although this list is in no way complete or comprehensive enough):

Building LNG Tankers in a Shipyard

Anatomy of Dominance: How China Engineered its Maritime Ascendancy & Learning Lessons

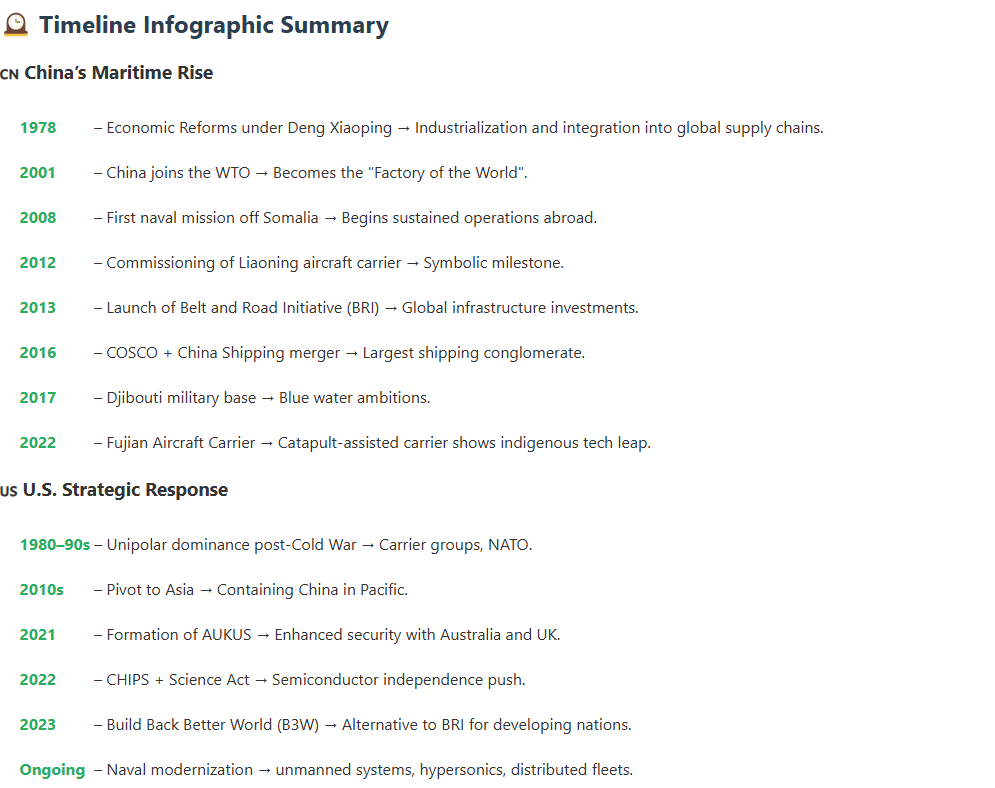

China's rise to the pinnacle of the global maritime industry was not an organic market development but the outcome of a meticulously planned, patiently executed, and state-driven strategy spanning nearly three decades (from approximately 1995). Understanding the interlocking components of this strategy is crucial to grasping the depth of China's current dominance and the scale of the challenge facing the United States and its allies.

State-Directed Vision & Long-Term Ambition

From the early 2000s, Chinese leadership identified maritime industries as critical pillars for national economic development and security. Successive leaders, from Zhu Rongji to Hu Jintao and Xi Jinping, articulated consistent national goals: China must become a "Strong Maritime Nation," a "Strong Shipbuilding Nation," and a "Strong Shipping Nation." This was explicitly linked to broader geopolitical ambitions, including Xi Jinping's "Chinese dream of national rejuvenation," framing maritime power as indispensable to China's status as a global power. This state-directed vision provided the overarching mandate for the policies and resource allocations that followed.

Parameter 1: Comprehensive Industrial Policy and Planning

China employed a top-down planning system to orchestrate its maritime ascent, cascading national objectives into actionable targets across industries and regions.

Centralized Planning Cycles: National Five-Year Plans (FYPs), starting significantly with the 10th FYP (2001-2005), coinciding with WTO accession, consistently prioritized maritime sectors. Overarching strategic initiatives like "Made in China 2025" (MIC2025) and the "Innovation-Driven Development Strategy" (IDDS) further directed resources and technological focus towards advanced maritime capabilities.

Sector-Specific Targeting: Numerous industry-specific plans set granular, quantitative targets for:

Shipbuilding: Overall production volume (e.g., aiming for world leadership by 2015/2020), market share (explicitly targeting 35% by 2011, later pushing well beyond 50%), revenue, and export volume.

High-Value & Specialized Vessels: Aggressive market share goals were set for complex ships. For example, MIC2025 targeted 40% global market share for maritime engineering equipment and 50% for high-technology ships by 2025. Green shipbuilding is a recent focus, with targets aiming for 50% market share in green-powered vessels by 2025.

Domestic Content: Mandates to increase the percentage of Chinese-made components installed on Chinese-built ships (e.g., targeting 80-85% for marine equipment by 2020/2025).

Maritime Engineering: Targets for offshore equipment market share (e.g., aiming for 40% by 2025).

Consolidation and Control: Policies actively encouraged the consolidation of the fragmented shipbuilding industry. This included state-directed mergers, most notably the 2019 recombination of CSSC and CSIC into a state-owned behemoth, and the creation of a "Whitelist" of shipyards (initially 51, growing to 70) that received preferential state support, financing, and orders, accelerating the demise of smaller, less-favored yards.

Parameter 2: Massive and Integrated Financial Support & Leveraging

State finance has been perhaps the most critical enabler of China's strategy, deployed at scale and integrated across the ecosystem.

The State Financial Arsenal: China utilized a wide array of financial tools involving key actors:

Actors: State-Owned Commercial Banks (BoC, ICBC, CCB), Policy Banks (CEXIM, CDB), Export Credit Agencies (Sinosure), SOE Leasing Arms (dominant players like CDB Leasing, ICBC Leasing, Minsheng Financial Leasing, BoCom Leasing), Government Investment Funds, and local government financial vehicles.

Mechanisms: Direct subsidies, below-market loans via policy banks, extensive export credits (buyers' and sellers'), critically important state-backed Refund Guarantees (RGs) which removed default risk for shipyards enabling them to take orders with minimal upfront capital, state-directed equity infusions, debt relief/swaps, specific tax incentives (VAT rebates), and a rapidly expanding, state-supported leasing sector offering aggressive terms (high Loan-to-Value ratios, long tenors).

Scale and Impact: The financial support has been immense.

Statistic: CSIS estimated at least $132 billion in state support (subsidies + financing) flowed to shipbuilding and shipping from 2010-2018.

Statistic: Academic analysis estimated $91 billion in subsidies alone for shipbuilding between 2006-2013 (accounting for ~46% of industry revenue).

Statistic: Chinese state banks provided $127 billion in financing (loans/leasing) from 2010-2018 (CSIS).

Statistic: Favorable financing terms saved Chinese SOE shipbuilders/shippers over $100 million annually in borrowing costs compared to private firms (CSIS, 2019).

Strategic Leveraging: China skillfully used finance as a tool. State banks explicitly tied financing for foreign shipowners to requirements that vessels be built in Chinese yards. State-backed leasing arms became major shipowners themselves, providing captive demand for domestic yards.

Parameter 3: Operational Structures, Scale & Commercial Practices

China translated policy and finance into operational advantages.

SOE Structure & Focus: Post-1990s SOE reforms, coupled with the decision not to emulate the diversified chaebol (Korea) or keiretsu (Japan) models, allowed giants like CSSC to achieve immense focus and scale within the shipbuilding sector.

Economies of Scale: Massive domestic demand (driven by trade growth) and government support allowed yards to achieve huge production volumes, especially for standardized vessels, driving down unit costs. Large, integrated shipyard complexes (like Changxing Island) were developed.

Labor & Engineering: China leveraged its large workforce, often benefiting from lower labor costs compared to competitors (partially due to systemic factors like the Hukou system and weaker labor protections, as detailed later). Simultaneously, the state made massive investments in maritime engineering education.

Statistic: China graduated 4,211 shipbuilding specialists in 2024, compared to South Korea's 767 – a sixfold advantage (Joongang Ilbo via @Jukanlosreve).

Contractual & Market Practices: State backing enabled SOEs to offer aggressive pricing and contract terms, absorb higher commercial risk, and potentially operate below market cost to gain strategic share. State control over major cargo owners (SOEs) likely allowed direction of shipping contracts towards Chinese carriers, further supporting the ecosystem.

Parameter 4: Technology Acquisition & Strategic Learning

China systematically acquired foreign technology and expertise to rapidly close the capability gap.

Emulation & Best Practices: Leaders actively studied and adapted successful models from Japan and South Korea.

Example: Jiang Zemin’s pivotal 1995 visit to Hyundai Heavy Industries spurred efforts to learn the "Korean development model." This was the pivot. The seed planted in imagination, and executed to perfection (if viewed from today’s lens)

Targeted Technology Acquisition: Efforts focused on critical areas needed for high-value ships:

Licensing: Securing essential foreign technology, such as GTT's membrane containment systems for LNG carriers.

Joint Ventures (Historical): Previously used JVs with foreign partners, often involving implicit or explicit tech transfer arrangements.

Recruitment: Actively recruiting experienced foreign engineers, designers, and managers, particularly laid-off experts from South Korea during industry downturns, offering lucrative salaries.

Statistic: An estimated 10% (around 2,000) of laid-off South Korean shipyard workers moved to China after the 2008 crisis (Industry estimates via @Jukanlosreve).

Reverse Engineering & "Re-innovation": Adapting and improving upon acquired foreign designs and technologies.

Allegations: Persistent concerns regarding IP theft and industrial espionage benefiting maritime sectors.

Exploiting Competitor Crises: China strategically expanded investment and recruitment during periods when South Korean and Japanese shipbuilders faced financial hardship or restructuring (e.g., post-1997 Asian Financial Crisis, post-2008 Global Financial Crisis, post-2014 oil price collapse). These 3 events feel like a “postnote” almost, and yet - in my mind, having lived through the events directly - they were significant!

Parameter 5: Control Over Raw Materials & Components

Dominance required securing the supply chain for essential inputs.

Raw Material Control: State influence over giant domestic SOE steel producers like Baowu Steel ensured preferential access and potentially lower costs for vast quantities of marine-grade steel plate, a major cost factor in shipbuilding.

Domestic Content Targets: Industrial plans mandated increasing proportions of domestically produced marine equipment (engines, deck machinery, navigation systems etc.) on Chinese-built ships, aiming for 80-85% localization. This policy directly displaced foreign component suppliers.

Parameter 6: Vertical Integration Across the Value Chain

China extended its strategy beyond shipbuilding to control interconnected maritime logistics and infrastructure.

Ecosystem Control: State-owned or affiliated entities achieved dominance in:

Ports: Massive investment in domestic ports and strategic acquisition/operation of over 96 overseas port terminals (many via BRI), influencing global trade flows.

Logistics Data: Promotion of the state-sponsored LOGINK platform, now handling data for potentially half of global container traffic, displacing competitors like TradeLens and creating information advantages/dependencies.

Equipment Manufacturing: Near-monopoly production of shipping containers (CIMC, >95%), intermodal chassis (CIMC, >86%), and ship-to-shore cranes (ZPMC, ~80% of US market).

Synergies: This vertical integration allows China to potentially coordinate activities across shipping, ports, logistics, and shipbuilding for strategic advantage.

Parameter 7: Military-Civil Fusion (MCF) in Maritime

A cornerstone of China's strategy is the deliberate integration of its commercial maritime industries with its military modernization goals.

Dual-Use Production: Top commercial shipyards, especially within CSSC (designated Tier 1 & 2 by CSIS), actively build advanced warships (destroyers, cruisers, amphibious assault ships, aircraft carriers) alongside complex merchant vessels (LNG carriers, ULCVs).

Example: Satellite imagery (CSIS) shows PLAN warships under construction adjacent to commercial vessels (e.g., Evergreen containerships) at yards like Jiangnan and Longxue.

Resource Cross-Pollination:

Financial: Commercial revenues ($ billions from foreign orders) help absorb fixed costs, subsidize naval R&D, fund yard expansions, and lower the per-unit cost of warships.

Technological: Dual-use technologies acquired through commercial channels (e.g., marine engines licensed from Europe, advanced navigation systems, specialty materials, GTT LNG tech) are adapted for naval applications.

Workforce/Expertise: Skills, design capabilities, and project management experience are shared across commercial and naval projects.

Foreign Enablement: International companies purchasing ships, supplying components, licensing technology, or providing capital to these dual-use yards inadvertently contribute to China's naval expansion.

Statistic: Over 75% of production at Tier 1 & 2 CSSC yards (2019-2024) was for foreign buyers, including U.S. allies (CSIS).

Consolidated Outcome: Global Dominance and Strategic Advantage

The cumulative effect of these integrated strategies has been transformative:

Market Annihilation: China achieved and surpassed its goal of becoming the world's largest shipbuilder, holding over 50% market share and ~62% of the global orderbook. Key competitors in KR/JP have seen their shares significantly eroded, while the US commercial sector is negligible.

Value Chain Control: China exerts significant influence, if not outright control, over shipbuilding, critical components, finance, shipping operations (via COSCO/SOEs), global port networks, and logistics data.

Technological Ascent: China has rapidly moved up the value chain, now competing strongly in high-value segments like LNG carriers, ULCVs, and green vessels, leveraging acquired technology and domestic innovation.

Enhanced Naval Power: The commercial shipbuilding boom directly fuels the PLAN's rapid modernization and expansion, creating significant national security implications.

So, China's maritime dominance is not merely a result of market forces but a product of decades of state direction, massive resource allocation, strategic integration, and the leveraging of global systems to achieve national objectives.

The U.S. Maritime Reality: A Fragmented Base and Critical Gaps

While China executed its multi-decade strategy for maritime dominance, the United States experienced a starkly different trajectory. Once a global maritime powerhouse capable of outbuilding the world during World War II and pioneering innovations like containerization and early LNG transport, the U.S. maritime industrial base has significantly eroded. Today, it stands as a fragmented shadow of its former self, particularly in commercial shipbuilding, presenting a profound contrast to China's integrated and rapidly expanding ecosystem.

The State of U.S. Shipbuilding: Decline and Strain

The decline of the U.S. large commercial shipbuilding sector has been precipitous.

Market Share Collapse: From a meaningful position decades ago, the U.S. share of global commercial shipbuilding tonnage has fallen dramatically, registering less than 0.2% in recent years (compared to China's >50%).

Yard Closures: Since 2010 alone, at least three major U.S. shipyards primarily focused on commercial work (Bender Shipyard, Avondale Shipyard, Alabama Shipyard) have closed or suspended operations. Many yards capable of building large ocean-going merchant vessels have exited the market entirely over the last few decades.

Limited Output: The U.S. delivers very few large ocean-going commercial vessels annually. For instance, in 2024, U.S. yards delivered only four bulk vessels totaling less than 30,000 compensated gross tons (CGT), a minuscule figure on the global scale.

Even the naval shipbuilding sector, which receives significant government investment and priority, faces substantial headwinds. Despite being technologically advanced, the handful of U.S. yards capable of building major warships (aircraft carriers, submarines, destroyers) are plagued by:

Persistent Delays and Cost Overruns: Government Accountability Office (GAO) reports consistently highlight significant schedule slippages and budget increases across major naval shipbuilding programs. A 20-year, $21 billion plan to modernize the Navy's own public shipyards was found to be years behind schedule and vastly over budget after only completing the first few projects.

Workforce Shortages: The naval sector faces a critical lack of skilled tradespeople. Estimates suggest an additional 100,000 to 140,000 skilled workers are needed over the next decade just to meet submarine production demands, a gap unlikely to be filled under current conditions.

This strained industrial base, both commercial and naval, struggles to meet even current demands, let alone compete effectively on the global stage or provide the surge capacity needed for national security.

Gap Analysis – Identifying Critical U.S. Weaknesses

The overall decline masks specific, critical capability gaps across the entire maritime value chain when compared to the integrated ecosystems built by China and, to a lesser extent, allies like South Korea and Japan.

Specialized Vessel Expertise & Capacity: The U.S. lacks the recent experience, specialized workforce, and industrial capacity to build most types of large, complex commercial vessels competitively.

LNG Carriers: No large LNG carriers have been built in the U.S. for decades. There is a critical lack of recent production experience, yards certified for large-scale cryogenic work, and a workforce skilled in specialized cryogenic welding (9% Nickel steel, Invar alloys). Furthermore, the domestic supply chain for crucial inputs like Invar alloy (essential for membrane containment systems) is non-existent, forcing reliance on foreign sources. The U.S. is also dependent on foreign technology licenses, primarily from France's GTT, for the dominant membrane containment systems. Building these complex vessels requires expertise in integrating cryogenic systems, boil-off gas (BOG) management, and advanced propulsion, areas where the U.S. industrial base has limited recent commercial experience. Note: A 31 year LNG Carrier flagged American, and crewed by US mariners - the “American Energy” was acquired by Crowly and Naturgy in Dec 2024, to deliver US-sourced natural gas to Puerto Rico in March 2025 - the 1st US-flagged LNG Carrier serving Puerto Rico. But it has a long way to go in terms of building.

FPSOs/Offshore Platforms: While the U.S. has offshore expertise, capacity for constructing and integrating the massive topside processing modules and complex hull/mooring systems required for modern FPSOs is primarily located in Asian and European yards. Managing these multi-billion dollar EPCI (Engineering, Procurement, Construction, Installation) projects requires scale and project management capabilities currently lacking in the U.S. commercial sector.

ULCVs/Large Tankers: U.S. yards cannot compete on cost or delivery time due to the lack of economies of scale achieved through serial production, lower levels of automation, and less optimized yard layouts compared to leading Asian shipbuilders.

Offshore Wind Vessels (WTIVs): The U.S. is only just beginning to build purpose-built Wind Turbine Installation Vessels. Yards require significant upgrades to handle the size and weight of next-generation turbines and foundations. The first U.S.-built WTIV, the Charybdis, faced significant delays and reported costs exceeding $715 million, far higher than comparable vessels built in Asia, highlighting the challenges. Reliance on foreign designs and critical components (like heavy-lift cranes and jacking systems) remains high.

Critical Component Supply Chain: The domestic supply chain for key maritime components is severely weakened or non-existent for large vessels.

Engines: Lack of domestic manufacturing for large, low-speed marine diesel engines (especially modern dual-fuel LNG/Methanol types prevalent in new builds). Reliance on foreign manufacturers (e.g., MAN, Wärtsilä) or their licensees in Asia.

Cryogenic Systems: Limited domestic production of large-scale LNG cargo handling pumps, compressors, valves, and insulation systems.

Other Systems: Gaps exist in domestic supply for advanced navigation and automation systems, large propellers and thrusters, and specialized castings/forgings needed for large vessel construction.

Raw Material Sourcing: While the U.S. produces steel and aluminum, accessing the specific grades (cryogenic, high-tensile marine plate) and quantities required for large-scale shipbuilding at globally competitive prices is a challenge. Unlike China's state-influenced steel sector (e.g., Baowu Steel), U.S. yards operate in a market where specialized materials can be costly or have long lead times. There is no domestic production of Invar alloy.

Financing & Contracting Ecosystem: The U.S. lacks the robust, state-backed financial mechanisms that China uses to support its industry.

ECA Gap: The U.S. Export-Import (EXIM) Bank provides far less support to the maritime sector compared to Asian ECAs like China's CEXIM/Sinosure or Korea's KEXIM/K-Sure.

Private Finance Risk Aversion: Without strong government backing (like RGs or significant subsidies) or long-term charter commitments securing revenue, private finance for high-cost, high-risk commercial shipbuilding projects in the U.S. is scarce and expensive.

Contracting Experience: Limited recent experience in structuring and managing the complex, multi-billion dollar, multi-ship contracts common for types like LNG carriers.

Workforce: Beyond the overall shortage of skilled trades (welders, pipefitters, electricians), there's an acute deficiency in specialized skills vital for advanced shipbuilding: certified cryogenic welders, technicians trained in installing and commissioning complex LNG/dual-fuel systems, digital design experts proficient in modern shipbuilding software, and naval architects experienced in optimizing designs for manufacturability and efficiency at scale. An aging workforce exacerbates this problem.

Cost & Pricing Disadvantage: The culmination of these gaps results in significantly higher costs for U.S.-built ships.

Statistic: Estimates consistently place the cost premium for a U.S.-built vessel at 35-40% or higher compared to a South Korean or Chinese equivalent. This gap is driven by higher labor rates, lower productivity due to lack of scale and automation, higher material and component costs due to supply chain fragmentation, and potentially higher regulatory compliance burdens.

Consequences: Economic Stagnation and National Security Risk

The erosion of the U.S. maritime industrial base carries severe consequences:

Economic Loss: Foregone opportunities for high-paying manufacturing jobs, reduced contribution to GDP, diminished export potential for complex maritime goods and services.

National Security Vulnerabilities:

Sealift Deficit: Insufficient U.S.-flagged commercial vessels and domestic shipbuilding capacity to meet military sealift requirements for deploying and sustaining forces in a major conflict. This necessitates reliance on foreign-flagged vessels, which may not be available or reliable in a crisis.

Repair & Sustainment Bottleneck: Limited dry dock capacity and workforce hinders the Navy's ability to maintain fleet readiness and repair battle damage promptly. The "Empty Bins" scenario described by CSIS, where the industrial base cannot keep pace with wartime consumption/losses, becomes a critical vulnerability.

Supply Chain Dependence: Reliance on foreign (potentially adversary) sources for critical naval components and materials poses unacceptable risks.

Deterrence Impact: A visibly weakened industrial base diminishes the credibility of U.S. power projection and sustainment capabilities, potentially emboldening adversaries.

In essence, the decline of the U.S. commercial maritime sector is inextricably linked to its national security posture. The gaps identified are not merely commercial challenges; they represent strategic vulnerabilities that China's targeted dominance actively exploits and exacerbates.

Charting a New Course: A U.S. Strategy for Maritime Revitalization

China's comprehensive, state-driven ascent has fundamentally reshaped the global maritime landscape, leaving the U.S. industrial base weakened and strategically vulnerable. Reversing this trend and rebuilding American maritime strength requires more than incremental adjustments; it demands a sustained, integrated national strategy with clear objectives, robust funding, international cooperation, and a willingness to employ targeted policy levers. This strategy must be realistic, focusing on strategic resilience, alliance, and competitiveness rather than attempting to mirror China's sheer scale in the near term.

Defining Strategic Objectives for a Maritime Renaissance

A successful U.S. strategy must be guided by clear, achievable goals that address both economic needs and pressing national security requirements:

Counter China's Military-Civil Fusion (MCF) & Unfair Practices: While I believe the road to domination should be paved with strategic innovation, and alliances, some of these activities are being put or are already in place. I.e., to actively disrupt the flow of capital, technology, and commercial revenue that fuels China's naval modernization via its dual-use shipyards. Level the playing field by addressing subsidies and non-market advantages.

Reduce China's Harmful Market Dominance: Whilst this has also been looked into i.e. to implement measures to curb China's overwhelming market share (currently >50% shipbuilding, ~62% orderbook), fostering a more balanced and competitive global market, I believe strategic innovation and building alliances will do more. This includes creating viable alternatives for global shippers.

Rebuild Minimum Essential Domestic Capacity: Focus on restoring sufficient U.S. shipbuilding and repair capacity to meet critical national security needs (e.g., Navy sealift requirements, battle damage repair, Jones Act fleet recapitalization) and ensure a baseline level of industrial resilience. Aiming for a modest but strategic market share (e.g., 5%) is more feasible than attempting to match China's volume.

Develop Specific Competencies: Target investment and training to rebuild expertise in constructing and maintaining specific complex vessel types (e.g., LNG carriers, offshore wind vessels, next-generation tankers/containerships, naval auxiliaries) and producing critical components (advanced propulsion, cryogenic systems).

Foster Allied Capacity ("Friendshoring"): Actively support and coordinate with key allies, particularly South Korea and Japan (holding ~34% and ~10% of the 2024 global orderbook share respectively), as well as European partners, to expand non-Chinese shipbuilding capacity and create resilient, diversified supply chains.

Secure Critical Supply Chains: Reduce dependence on China for essential raw materials (specialized steel, alloys), components (engines, electronics), and logistics platforms (data).

Achieve Technological Leadership: Focus R&D efforts on next-generation maritime technologies (autonomy, green fuels like ammonia/hydrogen, advanced materials, digital shipbuilding) where the U.S. and its allies can potentially leapfrog current Chinese advantages.

Ensure Economic Viability & Minimize Burdens: Design policies that achieve strategic goals efficiently, minimizing undue economic costs on U.S. consumers and businesses and ensuring allied buy-in through targeted, rather than overly broad, measures.

Policy Levers and Recommendations: An Integrated Approach

Achieving these objectives requires deploying a coordinated set of policy tools across multiple fronts:

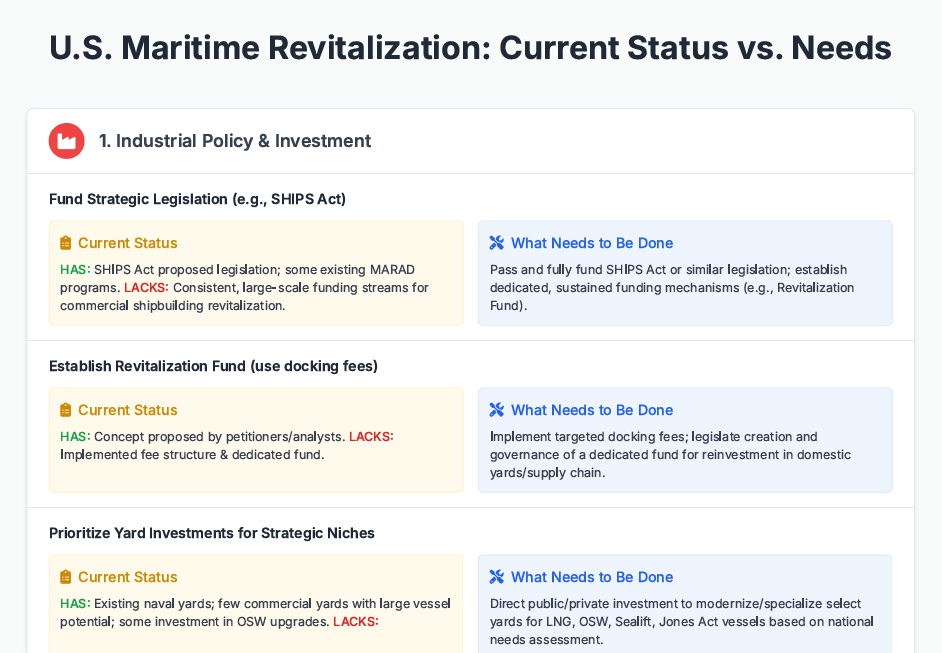

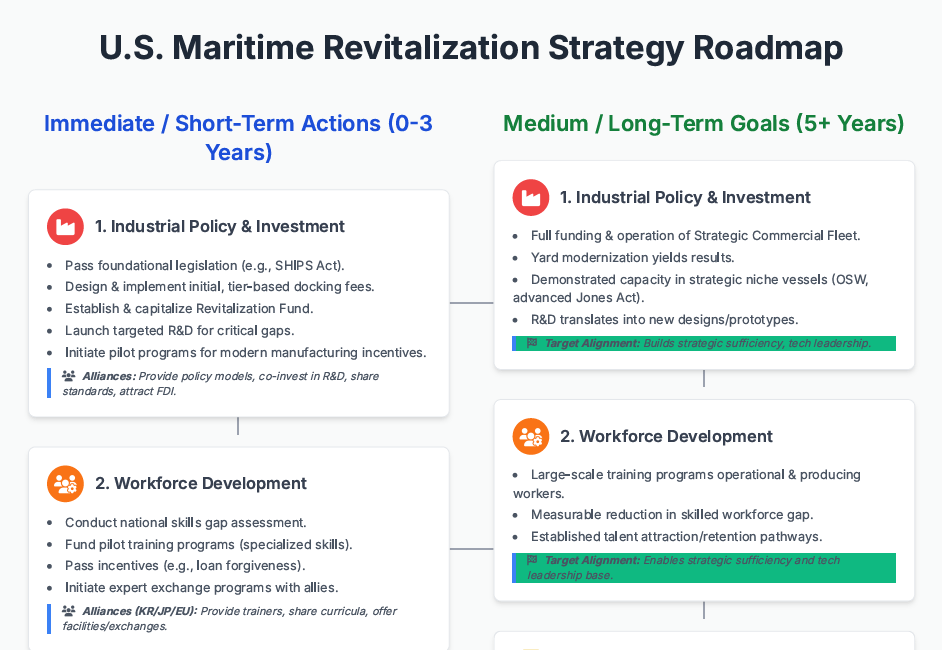

1. Targeted Industrial Policy & Investment

Fund Strategic Legislation: Fully fund and implement enacted legislation like the SHIPS for America Act, focusing on its provisions for a Strategic Commercial Fleet, shipyard investment tax credits, loan programs, and workforce development. Explore additional legislative authorities as needed.

Establish Revitalization Funding: Utilize revenue generated from proposed tier-based docking fees on Chinese-built vessels to capitalize a dedicated "U.S. Commercial Shipbuilding Revitalization Fund" for targeted domestic investments.

Prioritize Yard Investments: Direct public funds and incentives towards modernizing and potentially specializing U.S. yards capable of building vessels critical for national security (sealift, naval auxiliaries, OSW) and economic resilience (Jones Act, potentially niche exports like LNG carriers).

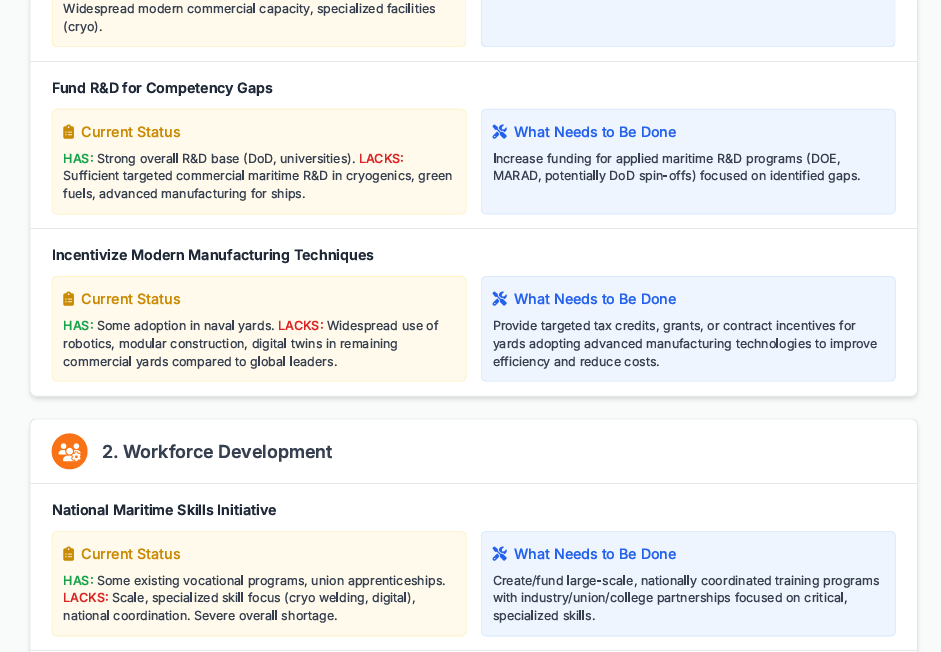

Spur Innovation & Modernization: Provide grants and tax credits specifically for adopting advanced manufacturing techniques (robotics, modular construction, digital twins) and for R&D focused on closing competency gaps (e.g., $500M DOE program for cryogenic H2 materials mentioned in CSIS sources).

2. Workforce Mobilization and Development

National Maritime Skills Initiative: Launch and fund large-scale vocational training, apprenticeships, and community college programs focused on critical, specialized skills – cryogenic welding certifications, digital design, complex pipefitting, systems integration, marine engineering for alternative fuels.

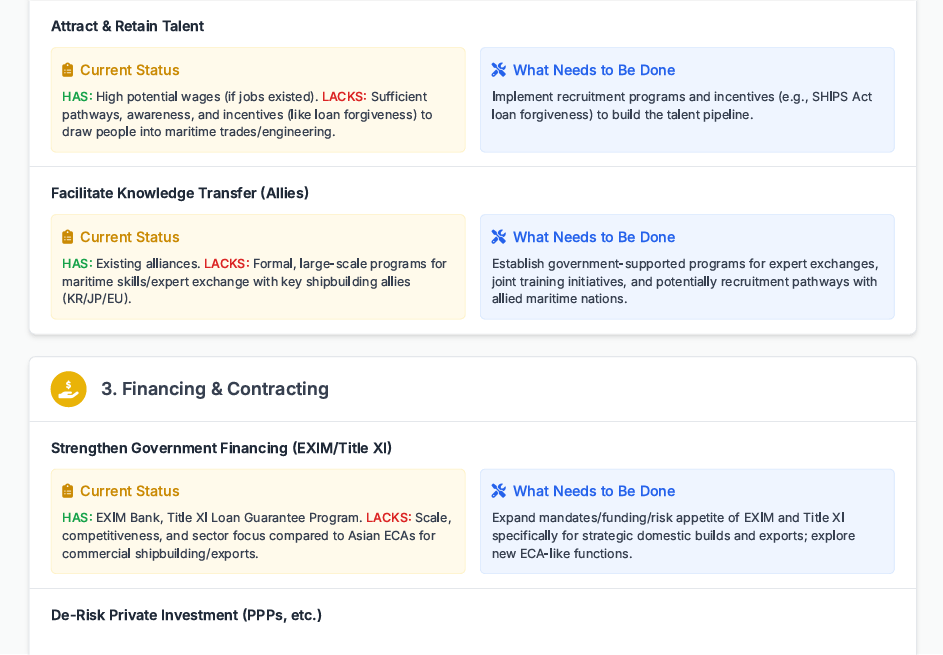

Attract & Retain Talent: Implement incentives (e.g., loan forgiveness as proposed in SHIPS Act) to draw skilled labor into the maritime trades and naval architecture/engineering fields.

Facilitate Knowledge Transfer: Support structured exchanges, training programs, and recruitment efforts involving experts from allied nations (KR, JP, EU) with established expertise in advanced commercial shipbuilding.

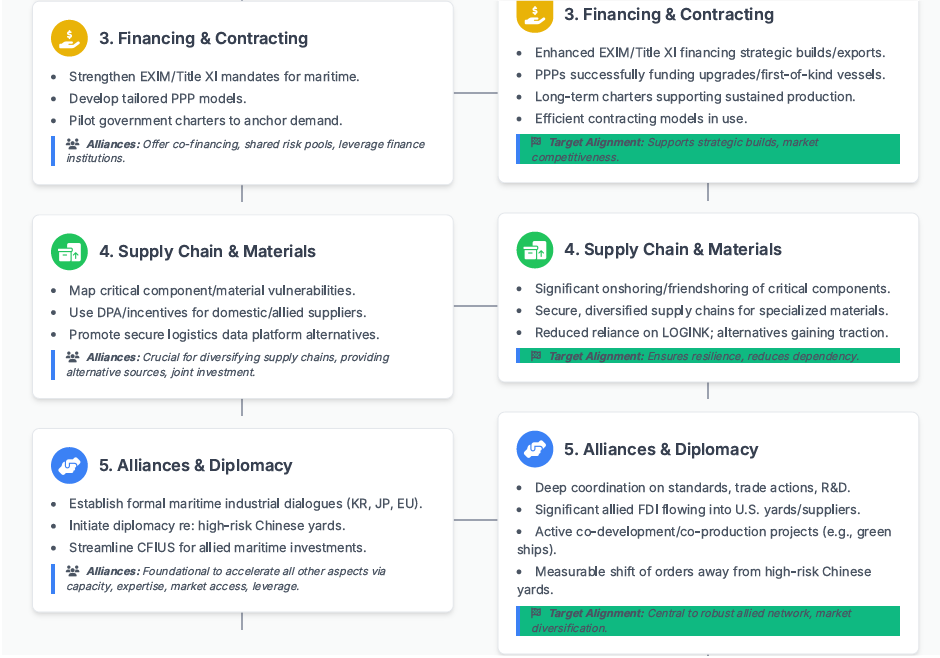

3. Financial & Contractual Innovation

Strengthen Government Financing Tools: Enhance U.S. Export-Import (EXIM) Bank programs and Maritime Administration (MARAD) Title XI loan guarantees, specifically targeting strategic vessel exports and domestic construction projects. Consider creating new ECA-like functions tailored to the capital-intensive nature of modern shipbuilding, offering terms more competitive with Chinese state banks.

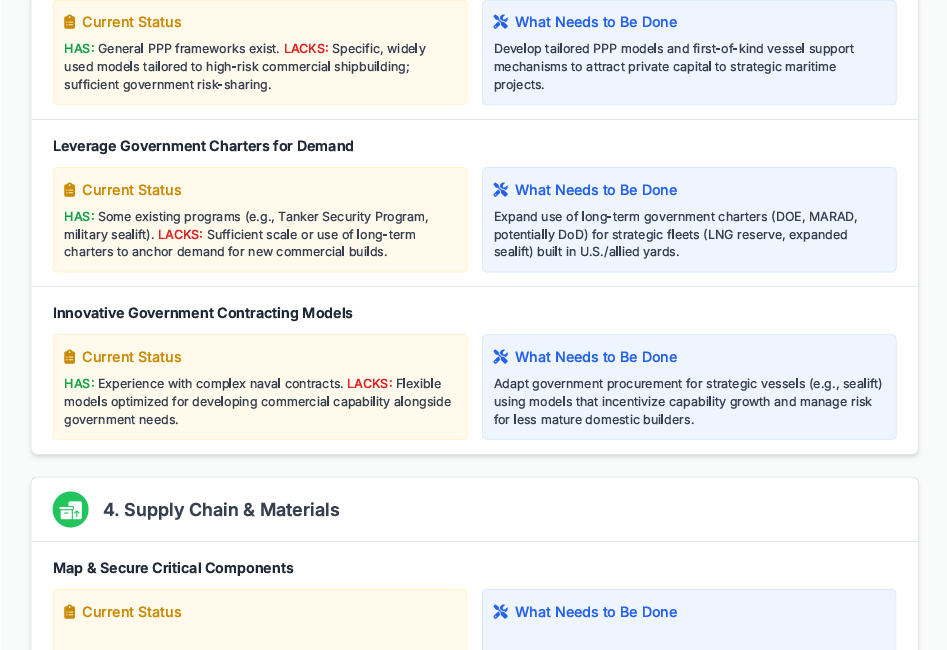

De-Risk Private Investment: Utilize Public-Private Partnerships (PPPs) for high-cost infrastructure (yard modernization) and first-of-kind vessel projects.

Leverage Government Cargo & Charters: Use long-term charter agreements for government-impelled cargo (expanding beyond current military/aid) or strategic fleet requirements (e.g., DOE strategic LNG reserve, Tanker Security Program) to provide predictable demand, enabling easier financing for new builds in U.S. or allied yards.

Innovative Contracting (Govt. Procurement): When procuring strategic assets like sealift vessels, employ contract models (e.g., variations of EPC, incentivized target cost) that balance risk, encourage innovation, and support the development of the domestic industrial base.

4. Supply Chain & Raw Material Security

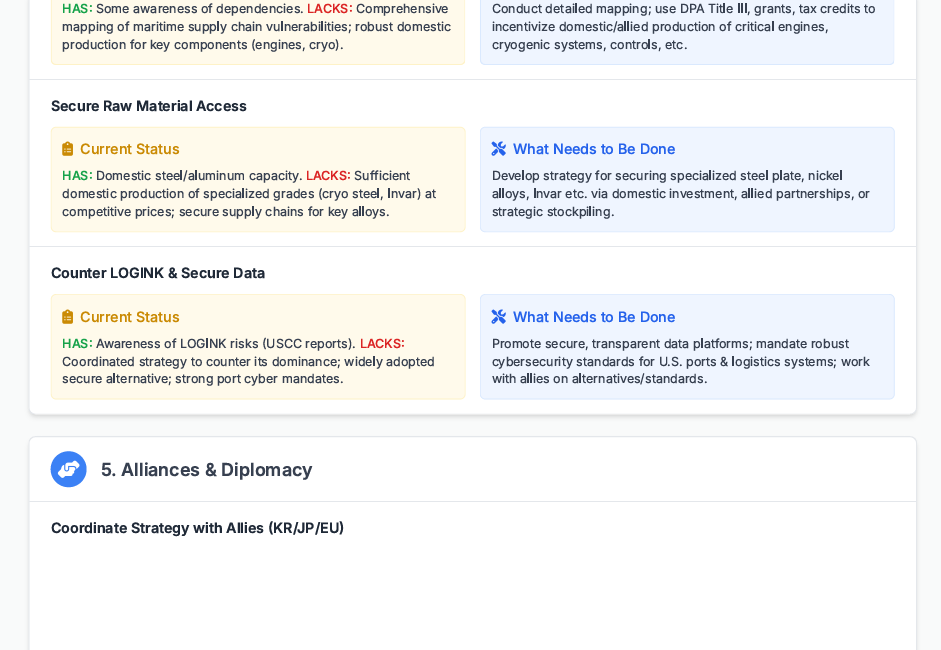

Map & Secure Critical Inputs: Conduct detailed mapping of supply chains for critical components (large engines, propulsion systems, cryogenic equipment, automation, specialized steel grades, Invar) and raw materials.

Incentivize Domestic/Allied Production: Use Defense Production Act (DPA) Title III, tax credits, and targeted subsidies to onshore or "friendshore" production of these critical inputs, reducing reliance on China.

Secure Raw Material Access: Develop strategies for securing reliable access to essential raw materials (nickel, specialty ores) through diplomatic agreements, strategic stockpiling, or support for domestic/allied extraction and processing.

Counter LOGINK: Actively promote secure, transparent, market-based logistics data platforms; mandate stringent cybersecurity standards for U.S. ports and interfacing systems; work with allies on alternative data-sharing standards.

5. Alliance-Based "Friendshoring" & Diplomacy

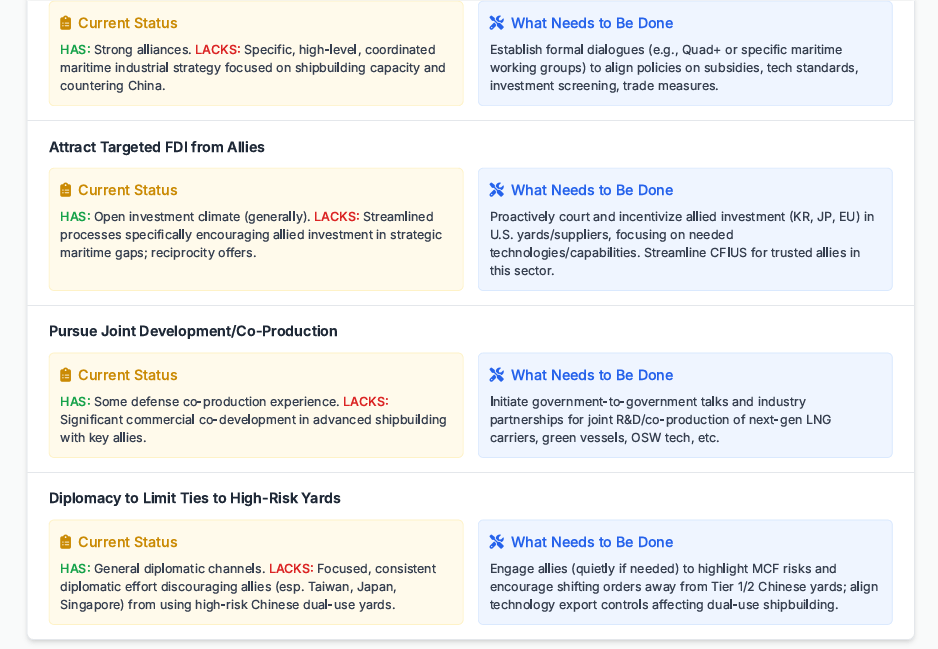

Coordinated Strategy: Establish formal dialogues and coordinate policies with key shipbuilding allies (South Korea, Japan, key EU nations) on technology standards, fair competition practices, countering Chinese subsidies, and reciprocal investment.

Attract Targeted FDI: Streamline CFIUS review processes for trusted allies investing in U.S. yards or critical component manufacturing, specifically targeting investments that fill identified capability gaps (e.g., Korean expertise in LNG containment, European leadership in green propulsion). Offer reciprocal investment opportunities.

Joint Development: Pursue collaborative R&D and potential co-production agreements for next-generation vessels (e.g., ammonia/hydrogen carriers, advanced OSW vessels, potentially common designs for naval auxiliaries).

Diplomatic Pressure: Use targeted diplomacy (potentially quiet/informal initially) to discourage allies from procuring vessels from or transferring sensitive dual-use technology to the highest-risk (Tier 1 & 2) Chinese shipyards identified as supporting the PLAN. Leverage existing alliances and security dialogues.

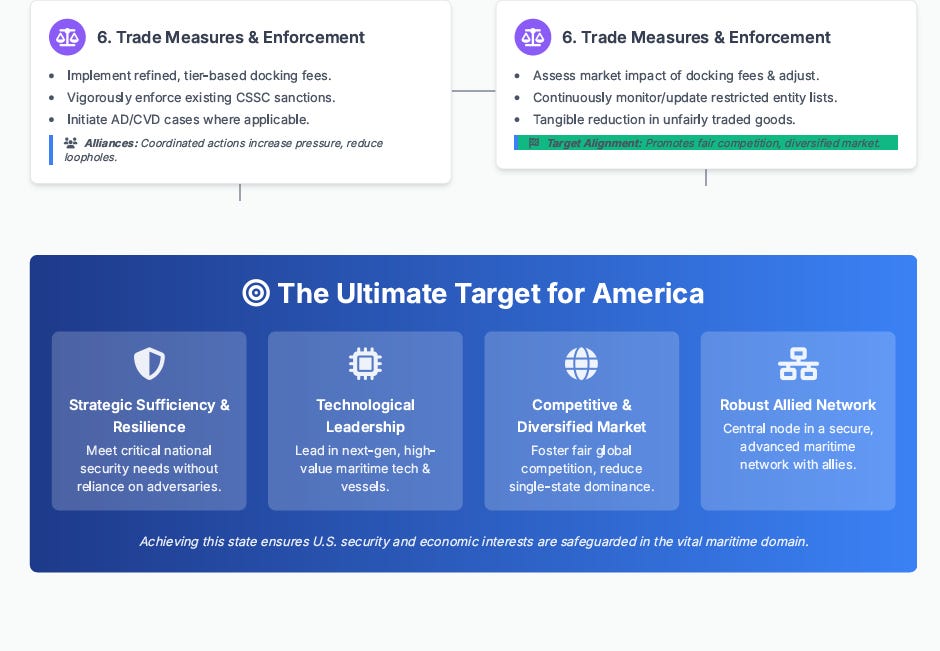

6. Calibrated Trade Measures & Enforcement

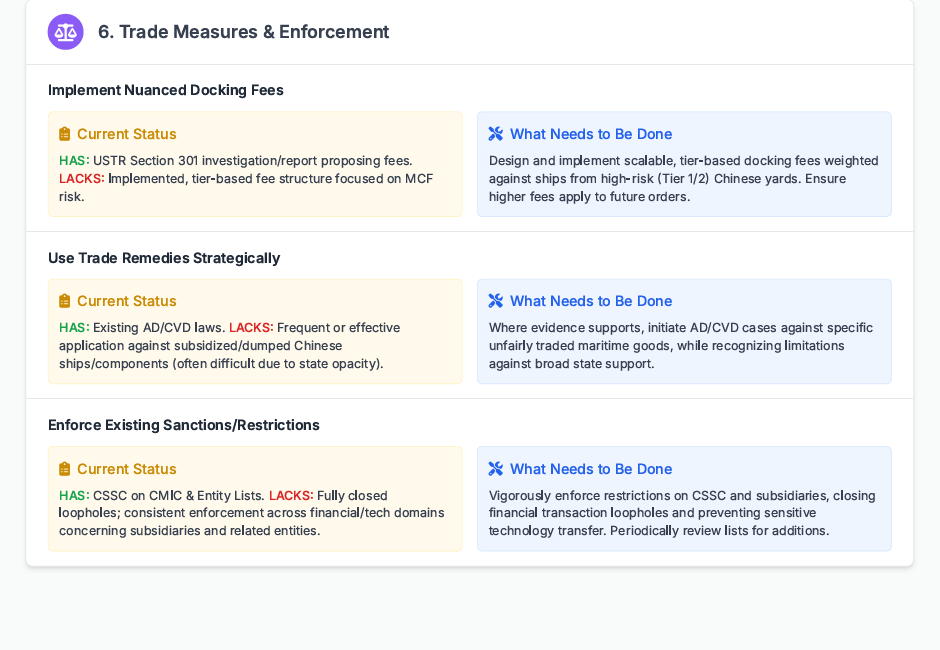

Implement Nuanced Docking Fees: Adopt a tier-based docking fee structure (as modeled by CSIS), imposing higher fees on vessels built in Chinese yards with direct naval links (Tier 1) or strong MCF connections (Tier 2), while applying lower or baseline fees to those from lower-risk yards. This targets the MCF threat more directly than a blanket fee. Ensure fees are higher for future orders post-implementation date to incentivize behavioral change.

Utilize Trade Remedies: Where appropriate and evidence allows, pursue anti-dumping and countervailing duty (AD/CVD) investigations against specific subsidized or dumped maritime products from China.

Enforce Existing Sanctions: Rigorously enforce existing U.S. Treasury (CMIC list) and Commerce (Entity List) restrictions targeting CSSC and its subsidiaries, closing financial loopholes.

This comprehensive set of recommendations, drawing from the analysis of China's success and U.S. weaknesses, provides a roadmap. Whilst many have been suggested, I may not always agree with them. Generally, It acknowledges the long-term nature of the challenge but offers concrete steps across policy, finance, industry, technology, and diplomacy to begin rebuilding American maritime strength and ensuring a more resilient and competitive global maritime order.

A Revitalization Strategic Roadmap

Can we take the lessons above and possibly apply a roadmap? Yes, of course! I believe one should be ready within the next 90 Days. In the meantime, here are some quick thoughts:

Any existing operator should be looking at the potential with glee! Given the likely strategic focus to be taken by the US, the business opportunities are going to be equally abundant! And I trust this is already being looked into. The early days will begin with fixed contracted builds, and then progress into more competitive opportunities. Whatever it is, the “slate is almost clean”, and who knows….anything is possible.

A National Maritime Strategy for a New Era

China's ascendance to the apex of the global maritime world is a landmark geopolitical and economic shift, achieved not through chance or simple market competition, but through a decades-long, state-directed, ecosystem-wide strategy. By meticulously integrating industrial policy, vast financial resources, strategic technology acquisition, control over key inputs and logistics networks, and the deliberate blurring of lines between its commercial and military sectors through Military-Civil Fusion, Beijing has constructed a maritime empire that now dominates global shipbuilding and exerts increasing influence over international trade flows. Most people have been beneficiaries of “the scale created in shipbuilding”, in terms of the cheaper goods landing on our shores, occupying our shelves. China faced challenges, it took the long strategic view, and yet - look at where they are now. Admirable! The next course to chart for the underdog should be just as elegantly built and scaled.

The consequences for the United States are stark. Its own maritime industrial base, particularly in commercial shipbuilding, has withered, leaving critical gaps in capacity, specialized skills, supply chain resilience, and financing mechanisms. This decline is not merely an economic concern; it translates directly into national security vulnerabilities (raised internally and discussed publicly), limiting America's ability to project power, sustain its naval forces, ensure the free flow of commerce during crises, and compete effectively on the global stage. The "Dragon's Wake" is reshaping the strategic landscape, demanding an urgent and coherent American response.

This analysis has shown that simply lamenting the decline or hoping for market forces to correct the imbalance is insufficient. Matching China's integrated strategy requires an equally holistic, sustained, and strategically focused U.S. national commitment. Revitalization cannot mean attempting to match China's sheer scale yard-for-yard or ship-for-ship in every category. Instead, success lies in a realistic, multi-pronged, allied, approach:

Addressing Foundational Gaps: Prioritizing investments to rebuild specific competencies in areas critical to national security and future economic competitiveness – including specialized vessel construction (LNG, OSW, Sealift, Jones Act), critical component manufacturing, advanced materials, and a highly skilled, modern workforce.

Countering Unfair Practices: Implementing targeted economic measures, like nuanced docking fees focused on high-risk Chinese yards, and enforcing existing restrictions to disrupt the MCF ecosystem and level the playing field.

Leveraging Alliances: Recognizing that the U.S. cannot do this alone, strategically partnering with key allies like South Korea, Japan, and European nations ("friendshoring") is essential to build alternative capacity at scale, share technological burdens, and create resilient supply chains complementing China's own.

Driving Innovation: Focusing R&D efforts on next-generation maritime technologies where the U.S. and its allies can establish and maintain a competitive edge, leapfrogging current areas of Chinese dominance where needed.

Ensuring Financial Viability: Creating innovative financing mechanisms (enhanced EXIM/Title XI, PPPs, government-backed charters) to de-risk private investment and provide the long-term capital needed for this generational undertaking.

This is undoubtedly a generational challenge. It will require significant public and private investment, sustained political will - transcending election cycles, and skillful diplomacy to mobilize a coalition of partners. The potential, purely from a business perspective, is lucrative! If done well. However, the cost of inaction – continued erosion of the industrial base, deepening strategic vulnerabilities, and effective cession of a critical domain to a potential geopolitical rival – is far greater. Perhaps diversification is not such a bad idea. By learning from the comprehensive nature of China's strategy and implementing an integrated response tailored to American strengths and allied capabilities, the United States can begin to turn the tide, ensuring its maritime resilience and securing its economic and national security interests on the world's oceans for the 21st century. The time to embark on this national maritime strategy for a new era is now - but it should also be well thought through. Strategy includes making friends, not enemies.

Update 30th April 2025 (post article write up):

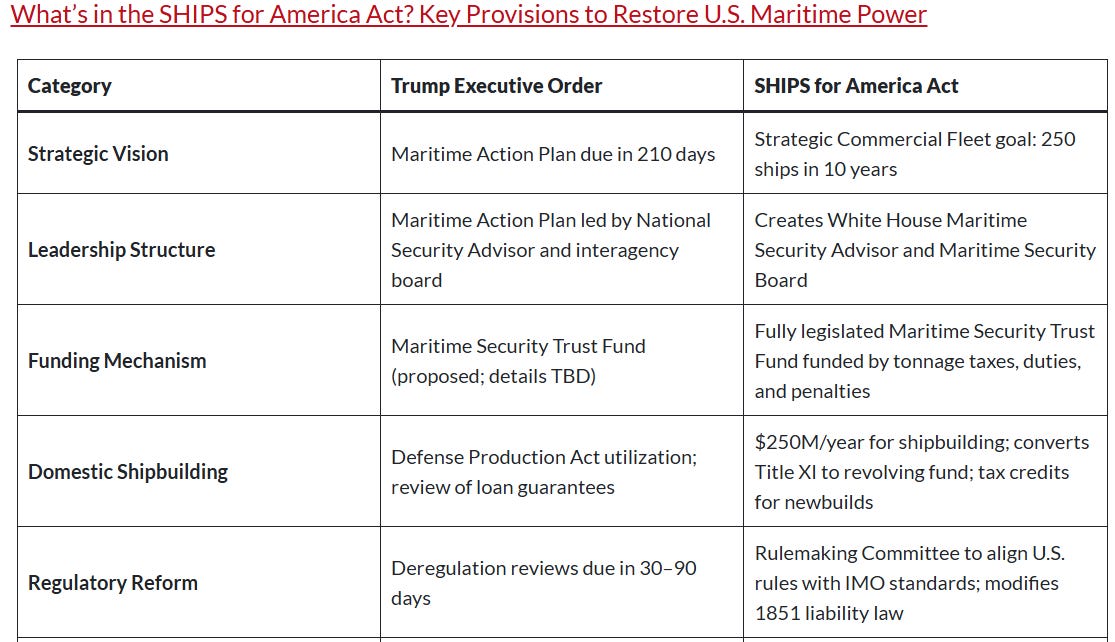

Charting A New Course: A Bipartisan Bill for the Ships Act 2.0 2025

Strategic Commercial Fleet goal: 250 ships in 10 years

→ Charting A New Course on Maritime Policy Ships For America's Act 2.0 -

https://gcaptain.com/trump-and-congress-chart-a-new-course-on-u-s-maritime-policy/

🚢 Bipartisan Bill introduced today 30th April 2025 - Ships For America's Act Provisions 2025 🚢

→ Key Provision which will drive Maritime Action Plan (MAP) due in 210 days to fulfill the → Strategic Commercial Fleet goal: 250 ships in 10 years ←

Core Strategy & Analysis Reports:

Center for Strategic and International Studies (CSIS) - Funaiole, Hart, Powers-Riggs (Main Report)

Title: Ship Wars: Confronting China’s Dual-Use Shipbuilding Empire & Murky Waters

Publisher: Center for Strategic and International Studies (CSIS)

Date: March 2025

Link: https://www.csis.org/analysis/ship-wars-confronting-chinas-dual-use-shipbuilding-empire

Link: https://features.csis.org/hiddenreach/china-shipyard-tiers/

YouTube:

Center for Strategic and International Studies (CSIS) - Funaiole, Hart, Powers-Riggs (Hill Brief)

Title: Confronting China’s Dual-Use Shipbuilding Ecosystem (Hill Brief)

Publisher: Center for Strategic and International Studies (CSIS)

Date: March 3, 2025

Link:

Office of the U.S. Trade Representative (USTR)

Title: Report on China’s Targeting of the Maritime, Logistics, and Shipbuilding Sectors for Dominance (Section 301 Investigation)

Publisher: Office of the U.S. Trade Representative

Date: January 16, 2025

Center for Strategic and International Studies (CSIS) - Blanchette, Hillman, McCalpin, Qiu

Title: Hidden Harbors: China’s State-backed Shipping Industry (CSIS Briefs)

Publisher: Center for Strategic and International Studies (CSIS)

Date: July 2020

Link: https://www.csis.org/analysis/hidden-harbors-chinas-state-backed-shipping-industry

Comparative Perspectives & Historical Context (X Threads & Articles):

Glenn Luk (@GlennLuk) X Thread on China Shipbuilding Rise

Source: X (formerly Twitter) Thread

Date: Started April 20, 2025

Link (Target Post): https://x.com/GlennLuk/status/1913931229264593370

(Note: Includes analysis of SOE restructuring, captive demand, learning from competitors, contrast with KR/JP)

Jukanlosreve (@Jukanlosreve) X Thread on China Shipbuilding Rise

Source: X (formerly Twitter) Thread

Date: Started April 20, 2025

Link (Target Post): https://x.com/Jukanlosreve/status/1913854298552975787

(Note: Includes details on Jiang Zemin's 1995 visit, RGs, talent cultivation, tech acquisition, financial crises)

Marantidou, Virginia (Jamestown Foundation)

Title: Shipping Finance: China's New Path to Becoming a Global Maritime Power

Publisher: The Jamestown Foundation, China Brief Volume 18, Issue 2

Date: February 13, 2018

Link: https://jamestown.org/program/shipping-finance-chinas-new-tool-becoming-global-maritime-power/

LNG Vessel Specific Sources :

American Bureau of Shipping (ABS)

Title: Guide for LNG Cargo Ready Vessels

Date: September 2019 (cited version)

Climate Analytics

Title: LNG shipbuilding industry heading to huge oversupply (Press Release/Report)

Date: (Date not specified, likely 2023/2024)

Link: https://climateanalytics.org/press-releases/lng-shipbuilding-industry-heading-to-huge-oversupply

OECD (Organisation for Economic Co-operation and Development)

Title: Report on China’s Shipbuilding Industry and Policies Affecting It

Publisher: OECD Publishing

Date: April 2021

Link: https://www.oecd.org/en/publications/report-on-china-s-shipbuilding-industry-and-policies-affecting-it_bb222c73-en.html (Cited extensively in USTR report)

OECD (Organisation for Economic Co-operation and Development)

Title: Ship Finance Practices in Major Shipbuilding Economies (OECD Science, Technology and Industry Policy Papers)

Date: August 2019

Link: Per above

Erickson, Andrew & Collins, Gabe (Orbis / FPRI)

Title: Beijing’s Energy Security Strategy: The Significance of a Chinese State-Owned Tanker Fleet

Publisher: Orbis, Volume 51, Issue 4 (Foreign Policy Research Institute)

Date: Fall 2007

Link: https://www.andrewerickson.com/wp-content/uploads/2010/11/Chinas-New-Tanker-Fleet_Orbis_Fall-2007.pdf

Oates, Kevin (Marine Money Asia)

Title: Ship Finance in Asia (Presentation)

Publisher: Marine Money Asia Pte. Ltd

Date: June 2014

Link: https://thecoalhub.com/wp-content/uploads/attach_535.pdf

Additional Supporting Sources (Cited within provided docs or contextually relevant):

Clarksons Research: (Data Provider) - Frequently cited for market share, fleet size, orderbook, and pricing data. https://www.clarksons.com/research/

S&P Global Sea-web: (Data Provider) - Used extensively in CSIS reports for shipbuilding production data. https://www.spglobal.com/marketintelligence/en/solutions/sea-web-maritime-reference

Government Accountability Office (GAO): Reports on U.S. Naval Shipyard modernization and readiness. (Search GAO.gov for reports like GAO-23-106067 and GAO-22-105993).

MERICS (Mercator Institute for China Studies): Provider of analysis on China's value chain dominance. https://merics.org/en

A sad story, but not too different than the decline of nuclear reactor fabrication in the US. The massive Gen III nuclear components designed by Westinghouse, are now licensed to the Chinese. The only solution proposed by government is the Small or Modular reactor systems. These SMR designs could possibly be modified for ship propulsion, replacing the typical PWR reactors now used. The Russians are probably ahead of this since they have ice breakers that are nuclear. I think that is what Trump wants in a fleet of ice breakers to counter.

Yes, unfortunately democracy was not built for long term strategic moves, to dominate industries.... Even the CHiPs Act gets slaughtered. And therein lie all our predicaments.....like markets. Short term quarterly price driven, not long term value motivated